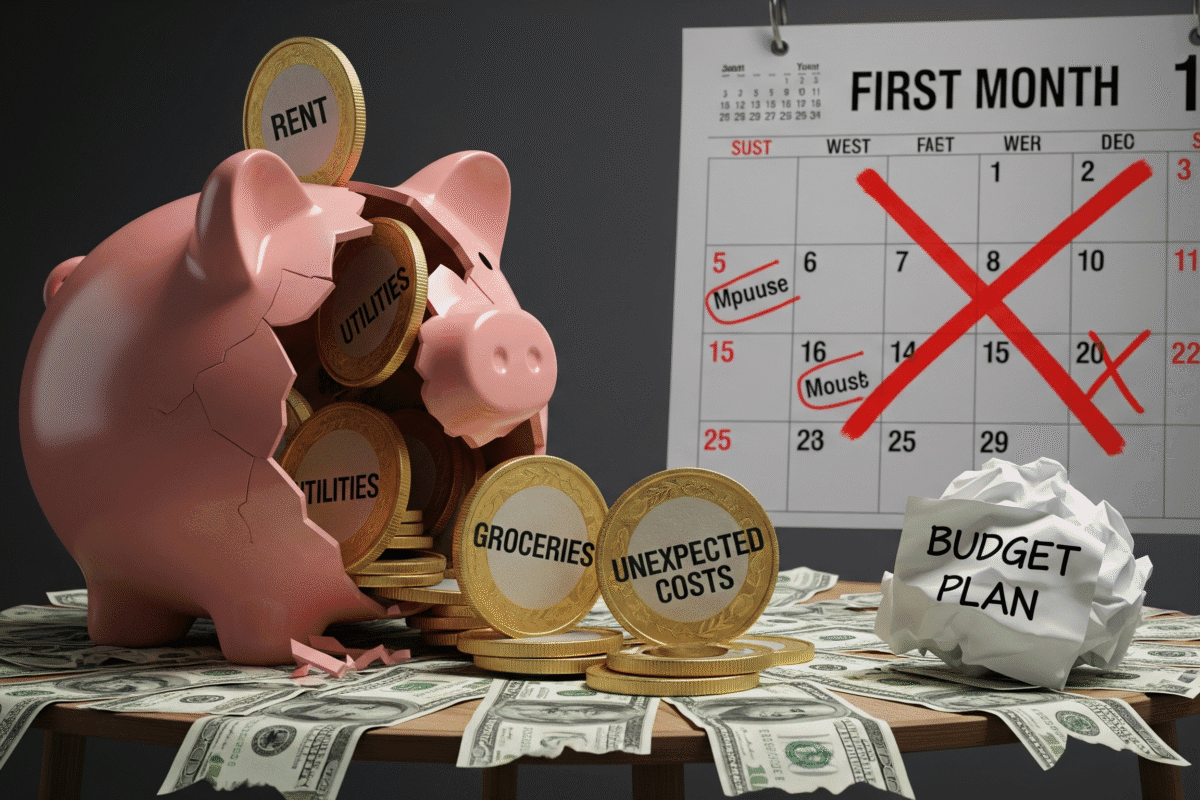

Why Most Budgets Fail in the First Month:

Why Most Budgets Fail in the First Month:

Personal budgeting techniques, TikTok finance instructors, and financial planning apps are all becoming increasingly popular in the US. However, research indicates that most budgets fail within the first month, even with this pervasive demand for financial control.

Only 41 percent of Americans actually stick to a budget, and many of those who do give up within the first 30 days, according to a recent U.S. Bank survey. The concerning failure rate begs the crucial question: What causes the majority of budgets to fail so fast, and what can be done to address the issue?

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

1. The Psychology of Ineffective Budgeting

The Issue of Willpower

Budgeting involves psychology as well as numbers. Budgeting, according to behavioral economics researchers, frequently fails because it depends on willpower, which is a finite resource. Decision fatigue occurs when someone tries to make big spending cuts all at once. Willpower wears out at the end of the first month, and spending resumes.

The Conflict in the Reward System

Our brains are wired for instant gratification. Swiping a card for a latte, ordering takeout, or buying new clothes activates dopamine release. Budgeting, on the other hand, delays gratification for future rewards like savings or debt reduction. This neurological mismatch often sabotages early budgeting attempts.

Unrealistic Expectations

Many people start budgeting after a financial “wake-up call” such as high credit card bills or unexpected expenses. In an emotional rush, they create overly strict budgets that cut out every indulgence. While inspiring in theory, this “crash diet” style rarely lasts more than a few weeks.

2. Typical Budgeting Errors That Cause Failure

Mistake 1: Ignoring Small Expenses

The classic “latte factor” still matters. A $5 coffee, $15 lunch, or $10 subscription may seem minor, but together they erode budgets quickly. People often underestimate how small expenses add up, making the first-month breakdown almost inevitable.

Mistake 2: Overcomplicating the Process

Many new budgeters download multiple apps, spreadsheets, and tracking tools. Instead of clarity, they face confusion. When budgeting feels like a second job, people abandon it quickly.

Mistake 3: Forgetting Irregular Expenses

Unexpected costs like birthdays, car repairs, or annual insurance premiums can destroy a budget. Since these aren’t monthly, people forget to plan for them—leading to overspending and frustration.

Mistake 4: No Emergency Cushion

Any unforeseen cost, such as a flat tire or hospital bill, can quickly destroy a budget if there is no emergency reserve. This gives the impression that the budget has failed when, in fact, it lacked sufficient flexibility.

Mistake 5: Relying Only on Motivation

Though life happens—stressful workdays, family responsibilities, or temptations—motivation is high during the first week. The budget and motivation both decline in the absence of mechanisms to automate savings or restrict expenditure.

3.Economic Realities Making Budgets Harder

Growing Living Expenses

Inflation in the U.S. has made essentials like groceries, gas, and rent significantly more expensive. Even the best budget can break if income doesn’t keep up with living costs.

Stagnant Wages

While costs rise, wages for many Americans have remained flat. This financial squeeze leaves very little margin for savings or debt payments. People start budgets with good intentions but fail due to structural economic barriers.

Debt Pressures

With record-high credit card debt in the U.S. (over $1.3 trillion in 2025), many households spend a significant portion of income on interest payments. This makes budgeting even harder.

4. The First-Month Trap

Why just the first month? Experts say the honeymoon phase of budgeting ends quickly:

- Week 1: Excitement and fresh motivation.

- Week 2: First slip-ups occur (eating out, unexpected costs).

- Week 3: Guilt and frustration replace motivation.

- Week 4: Many abandon the budget altogether.

This cycle repeats because people treat budgets like temporary challenges instead of long-term lifestyle shifts.

5. Professional Views on Budget Errors

Financial Advisor’s quote

“Most budgets fail because they are flawed, not because people are bad with money. According to Sarah Johnson, a licensed financial advisor in New York, a budget should complement your lifestyle rather than interfere with it.

Behavioral Economist quote

“Delayed satisfaction is not ingrained in human nature. For this reason, behavioral finance researcher Dr. Daniel Roberts says, “small, automatic changes—like saving $20 a week without thinking—work better than strict manual tracking.”

6. How to Create a Budget That Lasts Past the First Month

Step 1: Get Started Easy

Follow the 50/30/20 rule:

- 50% for necessities (bills, groceries, and rent)

- 30% for wants (entertainment, dining)

- 20% for debt or savings

This keeps things clear and realistic.

Step 2: Automate Finances

- Set up automatic transfers to savings or debt payments. This removes willpower from the equation.

Step 3: Track Only What Matters

- Instead of tracking every penny, focus on 3–4 problem categories like dining out, groceries, or subscriptions.

Step 4: Build in Flexibility

- Allow for “fun money” each month. Deprivation leads to rebellion, while controlled freedom builds sustainability.

Step 5: Prepare for the Unexpected

- Add a sinking fund for irregular expenses like car repairs, holidays, or medical costs.

Step 6: Use Psychology to Your Advantage

- Visualize savings goals, set up small rewards for progress, and use apps that gamify the process.

7. Case Studies: Effective Budgets

Case Study 1: The Budget for a Single Parent

Lisa, an Ohio single mother, had already abandoned three budgets. She changed to a basic cash envelope system for eating and grocery on her fourth try. She reduced her credit card debt by thirty percent in just six months.

Case Study 2: The Lifestyle Budget of Tech Workers

Software developer David, 28, struggled with spreadsheets. Rather, he invested the excess cash and automatically rounded up purchases using an app. This created stress-free savings.

Case Study 3: The Retired Couple

John and Mary, both retired, realized they were underestimating travel and leisure costs. Once they built a flexible category for hobbies and trips, their budget stuck.

8. The American Budget’s Future

With the rise of AI-driven personal finance apps, smarter automation may reduce failure rates. Banks are already testing real-time spending alerts, AI-generated savings tips, and predictive expense tracking.

However, experts warn that technology alone won’t fix bad habits. The key remains: realistic expectations, flexibility, and consistency.

Conclusion

The truth is simple: Most budgets fail in the first month because they are too strict, too unrealistic, and too dependent on motivation. Economic realities make it harder, and human psychology resists restriction.

But failure isn’t permanent. By starting simple, automating finances, and embracing flexibility, individuals can turn short-lived budgets into lifelong financial strategies.

Why People Fail to Stick to Budgets: Common Mistakes and How to Overcome Them

Why People Fail to Stick to Budgets: Common Mistakes and How to Overcome Them