How Mortgage-Backed Securities Work Today?

How Mortgage-Backed Securities Work Today?

Mortgage-backed securities (MBS) remain one of the most influential financial instruments in the U.S. economy, shaping everything from mortgage rates to institutional investment portfolios to the stability of the banking system. Although most Americans never buy an MBS directly, the products play a central role in how lenders fund mortgages and how the housing market operates.

Today’s MBS market looks very different from the one that contributed to the 2008 financial crisis. Strict new regulations, stronger underwriting standards, government-backed guarantees, and increased transparency have reshaped the system. Yet, the same core idea remains: thousands of home loans packaged into bonds that investors around the world can buy.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

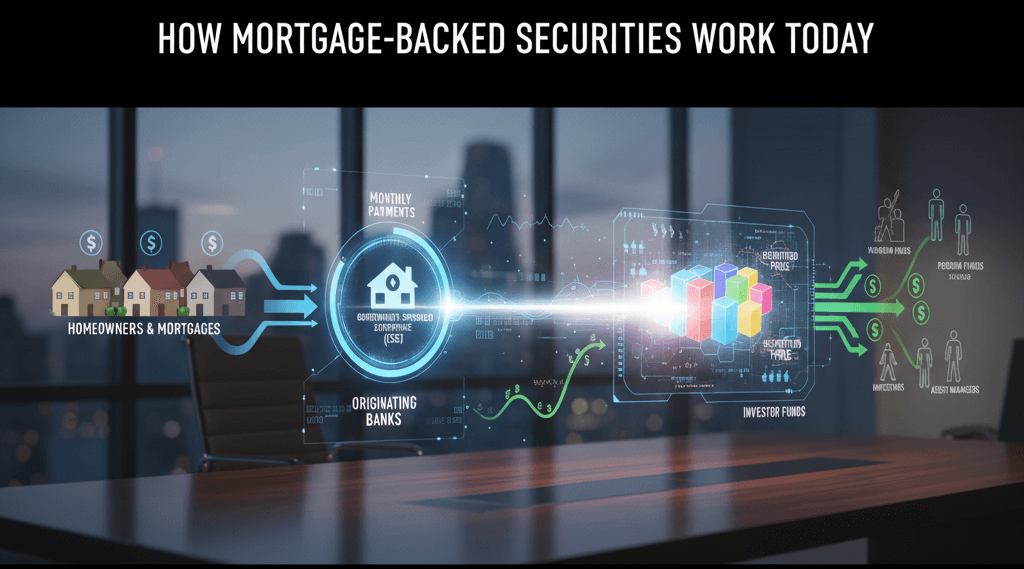

How MBS Are Produced in Today’s Market

Since the financial crisis, the securitization process has been more controlled and transparent. Typically, the steps consist of:

Pooling of loans

The loans are sold to a securitizing company like Fannie Mae or Freddie Mac after lenders amass thousands of comparable mortgages, usually categorized by interest rate, term, and credit factors.

The use of securities

Bonds are created from the loan pool. These securities are bought by investors, whose money returns to lenders so they can make new mortgages.

Monthly Payments and Maintenance

MBS investors receive the payments that borrowers continue to make to their mortgage servicer.

The Role of the Federal Reserve in the MBS Market

Since the 2008 crisis, the Federal Reserve has played an outsized role in supporting the MBS market.

Quantitative Easing (QE) and MBS Purchases

During crises, the Fed buys large amounts of agency MBS to stabilize the housing market and lower mortgage rates. Between 2020 and 2022, the Fed’s holdings reached record levels.

These purchases helped keep mortgage rates historically low — below 3% at one point — fueling a housing boom.

Quantitative Tightening (QT)

Starting in 2022, the Fed began allowing MBS to roll off its balance sheet. As a result:

- Mortgage rates surged

- MBS investors demanded higher yields

- Housing affordability declined

Who Buys Mortgage-Backed Securities Today?

The investor base for MBS is broad and global, making the securities highly liquid.

- Major MBS Investors

- Federal Reserve – although shrinking its holdings

- Banks and Credit Unions

- Pension Funds

- Insurance Companies

- Mutual Funds and ETFs

- Hedge Funds

- Foreign Central Banks and Sovereign Wealth Funds

Agency MBS attract conservative investors seeking stable income and low credit risk. Private-label MBS attract yield-seeking investors willing to analyze the underlying loans.

Current Trends in the MBS Market

As of today, several forces are shaping the outlook for mortgage-backed securities:

Fed Balance Sheet Reduction

With the Federal Reserve shrinking its MBS holdings, private investors must absorb more supply, influencing yields.

Tight Housing Inventory

Low for-sale inventory reduces mortgage origination volume, limiting new MBS issuance.

Growing Non-QM and Private-Label Issuance

As banks seek to serve borrowers who do not fit agency guidelines, private-label MBS have slowly regained momentum.

Renewed Interest in MBS ETFs

As bond yields climb, retail investors are increasingly turning to MBS exchange-traded funds for income.

Conclusion: How Mortgage-Backed Securities Work Today?

A fundamental part of the American financial system is still mortgage-backed securities. They supply the financing and liquidity needed to enable widespread homeownership. The fundamental structure is still the same, despite significant changes to the industry since 2008, including increased government engagement, stricter regulation, and higher underwriting criteria.

By connecting homeowners, lenders, Wall Street, and foreign governments into a single, interconnected ecosystem, MBS transforms millions of individual mortgages into a global investment commodity.

How U.S. Property Tax Caps Are Reshaping Housing Markets in 2025

How U.S. Property Tax Caps Are Reshaping Housing Markets in 2025