Behavioral Traps That Keep People in Debt:

Behavioral Traps That Keep People in Debt:

In America, debt is more than simply credit report figures. Millions of people are impacted by this behavioral, psychological, and emotional issue. From credit card balances to student loans, many households feel trapped in a cycle of borrowing and repayment.

But what really keeps people stuck in debt isn’t always lack of income — it’s the behavioral traps that lead to poor financial decisions. These traps are often invisible, rooted in psychology, habits, and social pressures.

In this in-depth report, we’ll explore the common behavioral traps that keep people in debt, why they are so powerful, and strategies to break free from them.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

The Debt Crisis in Quantitative Form

Let’s examine the broader picture before delving into specific actions.

- As of 2023, U.S. household debt reached a record $17 trillion, according to the Federal Reserve.

- Credit card debt alone crossed $1 trillion, with average annual interest rates above 20%.

- The average American household owes around $10,000 in credit card debt, not including mortgages or student loans.

- More than 60% of Americans live paycheck to paycheck, leaving little room to pay down balances.

Despite these numbers, many people repeat the same patterns — overspending, delaying payments, or taking on new debt to cover old debt. The reason? Behavioral traps.

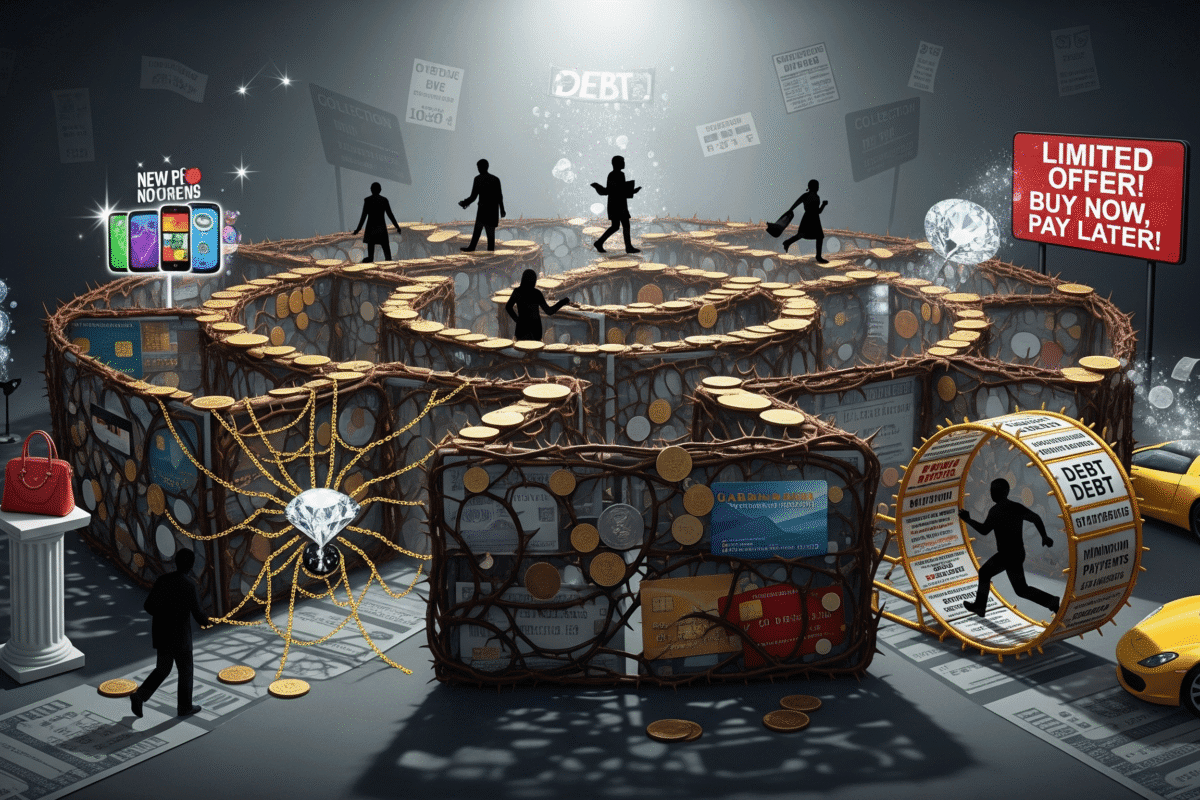

What Are Behavioral Traps?

A behavioral trap is a habitual action or thought pattern that seems harmless at first but leads to negative consequences. In the context of money, these traps keep people locked in debt cycles despite their desire to become financially free.

They are often subtle and hard to recognize, because they feel “normal.”

1. The Mentality of Minimum Payment

The minimum payment mentality is among the most prevalent pitfalls.

Many customers merely pay the minimal amount due on their credit card bills. After all, the account is still in excellent standing, so it feels like progress. However, in practice:

- Frequently, paying the minimum only covers interest and not principal.

- With minimum payments, a $5,000 balance at 20% APR might take more than 20 years to pay off.

- It is possible for interest charges to exceed the initial sum by two or three times.

This trap works because it offers short-term relief — a small payment today avoids immediate consequences, but it guarantees long-term debt.

2. Lifestyle Inflation: The Silent Trap

Lifestyle creep, sometimes referred to as lifestyle inflation, is when spending increases in tandem with income.

- A promotion leads to a new car.

- A shopping frenzy is triggered by a tax refund.

- A raise is justified by a larger home.

Instead of conserving money or paying off debt, people choose to improve their lifestyle. The result? Debt remains or grows.

Behavioral psychologists say this trap is linked to hedonic adaptation — the tendency to quickly get used to improvements and crave more.

3. Emotional Spending and Retail Therapy

Money is emotional. People often spend not out of need, but to:

- Relieve stress

- Celebrate small wins

- Escape sadness or boredom

Retail therapy provides a temporary dopamine boost. But the bill eventually arrives, and with interest, the emotional relief turns into financial pain.

This trap is especially powerful in the age of one-click shopping, buy-now-pay-later apps, and targeted online ads.

4. Social Comparison and Peer Pressure

Keeping up with the Joneses is more than a cliché — it’s a behavioral trap that drives consumer debt.

- Social media showcases luxury lifestyles, vacations, and expensive gadgets.

- Friends and family may encourage dining out, trips, or costly events.

- People fear appearing “behind” if they don’t match spending habits.

This trap thrives on status anxiety. Instead of living within their means, many stretch budgets — often using credit cards — to maintain appearances.

5. Optimism Bias: “I’ll Pay It Off Later”

Optimism bias makes people believe their future finances will be better than today’s.

- “I’ll get a raise soon.”

- “Next month I’ll save more.”

- “My tax refund will cover this.”

This idea supports taking on debt now in the hopes of improving financial circumstances later. Unfortunately, income increases often don’t materialize as expected, and debt snowballs.

6. Forgetting about Interest Rates

A lot of borrowers don’t realize how risky high interest is. Paying 18–25% interest on credit cards is essentially giving away wealth.

Yet surveys show a majority of Americans don’t know the interest rate on their cards. This lack of awareness creates a trap where balances linger for years, costing thousands.

7. The Debt Denial Trap

Avoidance is another psychological trap. Some people simply ignore bills because dealing with debt feels overwhelming.

- They delay opening mail.

- They avoid checking balances.

- They “hope it goes away.”

Denial provides short-term emotional comfort but leads to late fees, penalties, and damaged credit scores.

8. Anchoring to a Debt Number

When people focus only on one large debt — like a mortgage or student loan — they sometimes ignore smaller debts. This creates mental blind spots where small balances with high interest accumulate unnoticed.

Example: Someone may diligently pay their $300/month car loan while letting $5,000 in credit card debt spiral at 22% APR.

9. Overreliance on Future Income

Borrowers often assume tomorrow’s paycheck will solve today’s debt. But unexpected events — job loss, medical bills, inflation — can derail these assumptions.

This trap turns into a cycle: using debt as a bridge between paychecks instead of creating a safety net.

10. The “Debt Snowball” in Reverse

The debt snowball method (paying smallest balances first) helps people gain momentum. But many experience the reverse:

- They add new debt faster than they pay old debt.

- New balances cancel progress.

- Emotional discouragement sets in.

This behavioral trap makes debt feel endless, reducing motivation to even try.

Final Thoughts

Debt is not just a financial problem — it’s a behavioral challenge. The traps that keep people in debt are rooted in psychology, social pressure, and human habits.

Breaking free requires awareness, discipline, and mindset shifts. While the system is designed to encourage borrowing, individuals who recognize and escape these traps can move toward financial independence.

The Role of the Federal Reserve in World Finance: Global Impact and Future Outlook

The Role of the Federal Reserve in World Finance: Global Impact and Future Outlook