Why Homeownership Rates Differ by Race and Region?

Why Homeownership Rates Differ by Race and Region?

In the US, homeownership has long been regarded as one of the most potent catalysts for wealth accumulation. Home ownership has long been seen as a means of achieving upward economic mobility, communal stability, and financial security. However, homeownership is still unequally distributed among racial groups and geographical areas in spite of this objective. Concerns regarding equity, access, and economic opportunity in contemporary America are urgently raised by the enduring disparities.

As of recent national surveys, White Americans continue to achieve the highest homeownership rates, followed by Asian, Hispanic, and Black households, with Black families maintaining the lowest rates for decades. Similarly, regional variations—from the Northeast to the South to the West—reveal stark differences shaped by economic structures, housing supply, migration patterns, and state-level policy.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

The Present Racial Homeownership Disparity

There are notable differences in homeownership between racial and ethnic groupings in the United States, according to recent data.

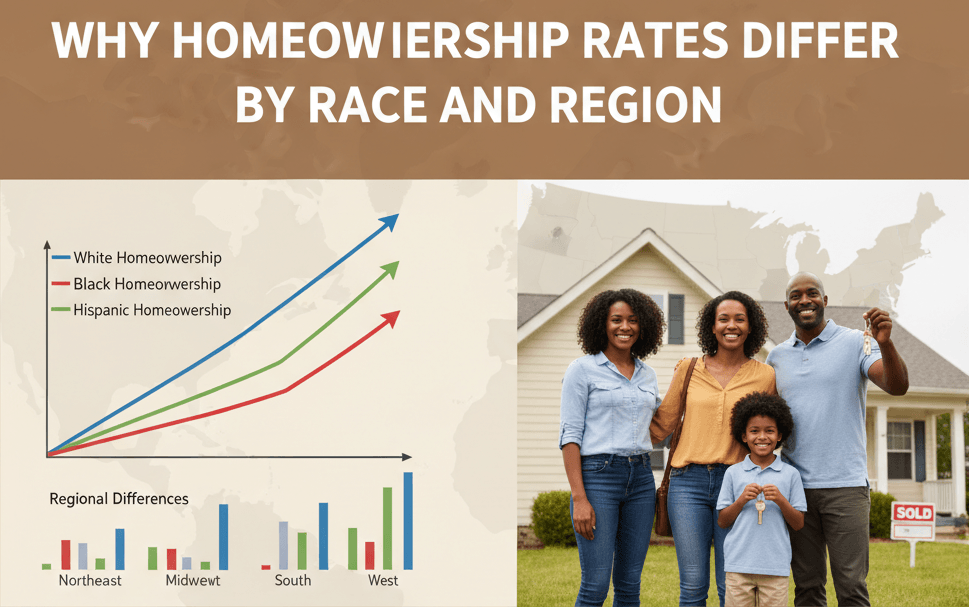

- Black Americans had a homeownership rate of 42.1% in 2019 compared to roughly 73.3% for non-Hispanic white Americans, a difference of more than 31 percentage points, according to USAFacts.

- Asian or Pacific Islander Americans reported a rate of 57.7%, Hispanic or Latino Americans reported a rate of 47.5%, and American Indian or Alaska Native households recorded a rate of 50.8%.

- The Black-White disparity has increased from 27% in 2013 to 28% in 2023, despite improvements in rates for all groups, according to the National Association of Realtors’ Snapshot of Race and Home Buying in America.

Progress Indications—and Caution

Not all of the news is negative. There are indications of progress, but difficulties still exist.

- Hispanic and Asian homeownership rates have reached all-time highs in recent years (Hispanic ~51.1%, Asian ~63.3%), according to the National Association of Realtors.

- Compared to other racial groupings, the Black homeownership rate increased at its fastest yearly pace in 2023; yet, the difference with White families is still substantial (~28 percentage points).

- These improvements demonstrate that progress is achievable, particularly with focused policy interventions, loan availability, and down payment support.

But:

- Improvements are brittle. Gains can be swiftly undone by economic downturns, increased mortgage rates, and low inventories.

- The benefits can remain unequal and unsustainable if systemic assessment bias, income inequality, and regional segregation are not addressed.

Structural and Historical Factors

Why are these gaps still present? America’s past and the systemic obstacles ingrained in housing policy provide a significant portion of the solution.

Segregation and Redlining

- Homeownership is still impacted by the history of redlining, the discriminatory practice of refusing insurance or mortgages to residents of communities with a high concentration of minority residents. For decades, these methods depressed home values and exacerbated racial segregation in Black and other minority areas.

- Even after the Fair Housing Act of 1968 made such discrimination illegal, its long-term effects remain entrenched in the housing landscape.

Bias in Appraisal

- Bias in property appraisals has historically devalued homes in majority-Black or minority neighborhoods. Lower appraisals make it harder to access credit, refinance, or leverage the equity that comes from homeownership.

- The racial wealth gap is exacerbated by these biased appraisals since properties in minority populations are frequently underestimated, which restricts the building of home equity.

Signs of Progress — and Caution

Not all of the news is negative. There are indications of progress, but difficulties still exist.

- Hispanic and Asian homeownership rates have reached all-time highs in recent years (Hispanic ~51.1%, Asian ~63.3%), according to the National Association of Realtors.

- Compared to other racial groupings, the Black homeownership rate increased at its fastest yearly pace in 2023; yet, the difference with White families is still substantial (~28 percentage points).

- These improvements demonstrate that progress is achievable, particularly with focused policy interventions, loan availability, and down payment support.

Conclusion: Why Homeownership Rates Differ by Race and Region?

The gap in homeownership rates by race and region in the U.S. is more than a statistical anomaly — it is a reflection of deep-seated inequities embedded in the country’s history, economy, and structural policies. While some progress has been made, particularly for Hispanic and Asian buyers, Black homeownership still lags behind by a wide margin.

Regional disparities further complicate the picture: where people live — city vs. suburb, Northeast vs. South — sharply shapes their chances of owning a home. These disparities cannot be divorced from historical practices like redlining, discriminatory lending, and appraisal bias, nor from economic realities such as income inequality and wealth gaps.

The Economics of Side Hustles: How the American Middle Class is Redefining Work

The Economics of Side Hustles: How the American Middle Class is Redefining Work