The Power of Asset Allocation:

The Power of Asset Allocation:

Asset allocation is a timeless notion in the volatile and fast-paced world of investing. While stock picking, crypto investing, and chasing “hot trends” often dominate headlines, the real driver of long-term wealth is not about predicting the next big winner—it’s about how you allocate your assets across different investment classes.

In 2025, when global markets are more connected, volatile, and technology-driven than ever, understanding the power of asset allocation has never been more critical. Whether you are a seasoned investor or just beginning your financial journey, the right allocation strategy can help you achieve financial independence, reduce risks, and secure steady returns.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

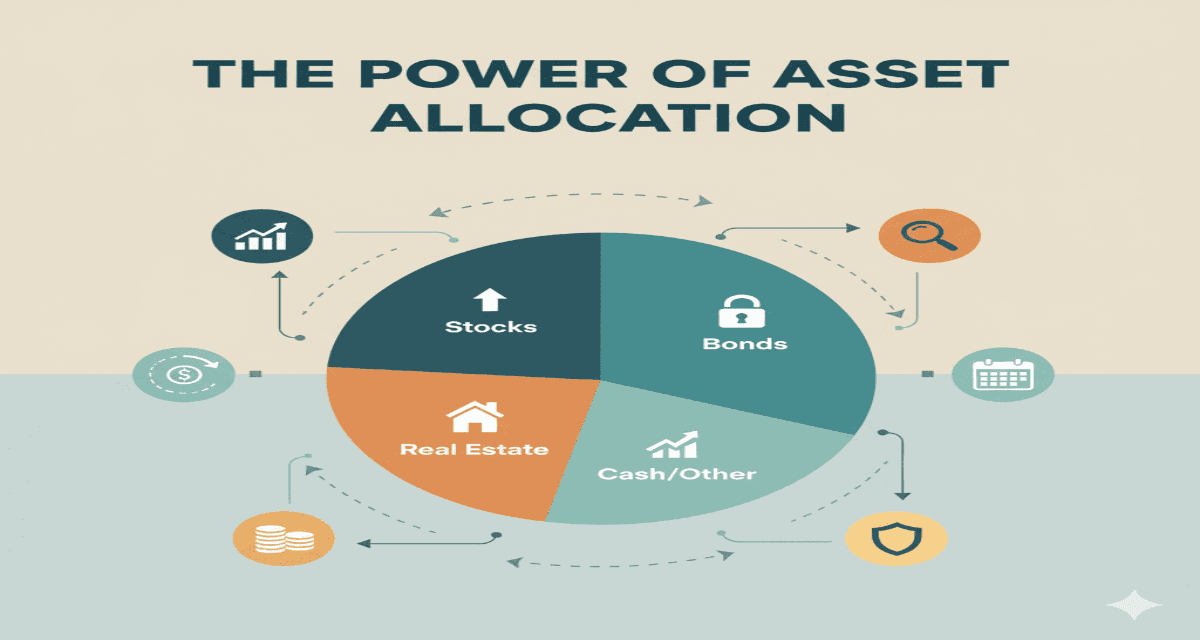

Asset Allocation: What is It?

The practice of distributing an investment portfolio among several asset classes, such as stocks, bonds, real estate, commodities, and cash equivalents, in order to balance risk and return in accordance with your financial objectives, time horizon, and risk tolerance, is known as asset allocation.

Asset allocation adopts a long-term strategic approach as opposed to market timing or speculating. It recognizes that no single asset class consistently outperforms, which is one of the most significant facts in finance.

For example:

- Although stocks have a significant volatility, they frequently yield high returns.

- Bonds provide stability and income but lower growth potential.

- Real estate offers long-term appreciation and rental income but is less liquid.

- Cash equivalents provide safety but may not keep up with inflation.

Why Asset Allocation Matters in 2025

The global financial landscape in 2025 is marked by several unique challenges and opportunities:

- Inflationary Pressures – Rising prices continue to erode purchasing power, making inflation-protected assets more valuable.

- Geopolitical Uncertainty – Ongoing conflicts and policy shifts drive market volatility.

- Technological Disruption – Artificial intelligence, blockchain, and clean energy reshape industries, offering new investment avenues.

- Interest Rate Movements – Central banks adjust policies that directly affect bond yields, stock valuations, and real estate markets.

In such an environment, putting “all eggs in one basket” is a risky gamble. A diversified allocation helps investors ride the highs of growth assets while cushioning against downturns.

The Science of Allocation of Assets

Numerous studies, including the famous Brinson, Hood, and Beebower (BHB) study, show that over 90% of a portfolio’s long-term returns are determined by asset allocation, not by individual stock picking or market timing.

This research underscores that how you allocate assets matters more than which individual assets you choose.

For instance:

- An investor with a 70% stock / 30% bond portfolio will generally see higher long-term growth compared to someone holding 100% bonds—but also more volatility.

- Conversely, an investor nearing retirement might prefer 40% stocks / 50% bonds / 10% cash for stability.

Important Asset Classes for 2025

Equities, or stocks

- Represent a company’s ownership.

- Provide high growth potential, especially in tech, healthcare, and renewable energy sectors.

- Volatile but essential for long-term wealth building.

Bonds (Fixed Income)

- Government and corporate bonds provide predictable income.

- Act as a hedge during stock market downturns.

- Interest rate changes significantly affect bond performance.

Real Estate

- Includes residential, commercial, and REITs (Real Estate Investment Trusts).

- Offers diversification beyond traditional securities.

- Acts as a hedge against inflation.

Commodities

- Gold, silver, oil, and agricultural products.

- Useful for hedging against inflation and geopolitical risks.

- Highly volatile and often speculative.

Money and Money Equivalents

- Savings accounts, money market funds, and Treasury bills.

- Provide safety and liquidity.

- Inadequate inflation protection, but helpful in an emergency.

Alternative Investments

- Includes cryptocurrency, hedge funds, and private equity.

- Less regulated and more risky, but it can increase profits.

Techniques for Astute Asset Distribution

Allocation Based on Age (The Rule of 100)

A classic rule suggests subtracting your age from 100 to determine the percentage of stocks in your portfolio. For example, at age 30, you might hold 70% stocks and 30% bonds.

Risk Tolerance-Based Allocation

Some investors are naturally risk-takers; others are risk-averse. Your portfolio should match your emotional and financial ability to withstand volatility.

Target-Date Funds

Ideal for retirement planning. These funds automatically adjust asset allocation as you approach a target date (like 2045).

Core-Satellite Strategy

Core: Passive investments like index funds or ETFs.

Satellite: Active investments in growth sectors or alternative assets.

Global Diversification

Investing beyond U.S. borders can capture growth in emerging markets and reduce home-country bias.

The Function of Rebalancing Portfolios

Over time, certain asset classes may outperform others, causing your allocation to drift away from its target. Rebalancing involves periodically realigning your portfolio back to its original structure.

For instance, if your goal allocation is 60% stocks and 40% bonds, and stocks rise to 70% during a bull market, you sell some stocks and purchase bonds to bring the allocation back into balance.

This process enforces buy low, sell high discipline and reduces emotional investing mistakes.

Asset Allocation for Different Life Stages

Investors in their 20s to 30s

- High stock allocation (70–90%).

- Pay attention to long-term compounding and growth.

Mid-Career (40s–50s)

- 50–60% stocks, 30–40% bonds, and 10% real estate make up a balanced portfolio.

- Prioritize growth while managing risk.

Nearing Retirement (60s–70s)

- Conservative allocation: bonds (50–60%), stocks (30–40%), cash (10%).

- Focus on income and capital preservation.

Retirees (70+)

- Bonds, dividend-paying stocks, and cash-heavy allocation.

- Emphasis on stability and predictable income.

Allocating Assets amid erratic markets

When markets swing wildly, allocation provides a safety net. For instance, during the 2020 pandemic crash, investors with diversified portfolios saw less damage compared to those fully invested in equities.

In 2025, geopolitical tensions, energy crises, and rapid technological shifts amplify uncertainty. Diversification across asset classes, geographies, and sectors ensures investors stay resilient.

Technology and the Future of Asset Allocation

Artificial intelligence (AI) and robo-advisors now help investors craft personalized portfolios using algorithms. Platforms like Betterment, Wealthfront, and Vanguard Digital Advisor provide low-cost, automated asset allocation based on individual risk profiles.

Additionally, blockchain-based assets and tokenized real estate are expanding the scope of asset classes available to retail investors.

Conclusion: Asset Allocation’s Real Power

Asset allocation is not about predicting the future—it’s about preparing for it. In 2025’s uncertain financial environment, a well-diversified portfolio tailored to your goals and risk tolerance is your best defense against volatility and your strongest tool for wealth creation.

By spreading risk, maximizing returns, and adapting to market conditions, asset allocation ensures investors stay focused on the big picture: building financial independence and security for the long run.

Whether you’re a millennial starting your investment journey or a retiree safeguarding your nest egg, remember this golden rule: It’s not about timing the market; it’s about time in the market—with the right asset allocation strategy.

The Impact of Childhood on Money Habits: How Early Experiences Shape Financial Futures

The Impact of Childhood on Money Habits: How Early Experiences Shape Financial Futures