The Economics of Private Credit Funds in U.S. Finance

The Economics of Private Credit Funds in U.S. Finance

Over the past ten years, there has been a subtle but significant change in the financial landscape of the United States. Private credit funds are an emerging entity that has been subtly changing the dynamics of corporate lending, even as traditional banking institutions continue to dominate the supply of credit to individuals and businesses. A burgeoning sector of the alternative credit market, private credit funds—also known as private debt funds—provide high-net-worth individuals and institutional investors with access to profitable lending options outside of the traditional banking system.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

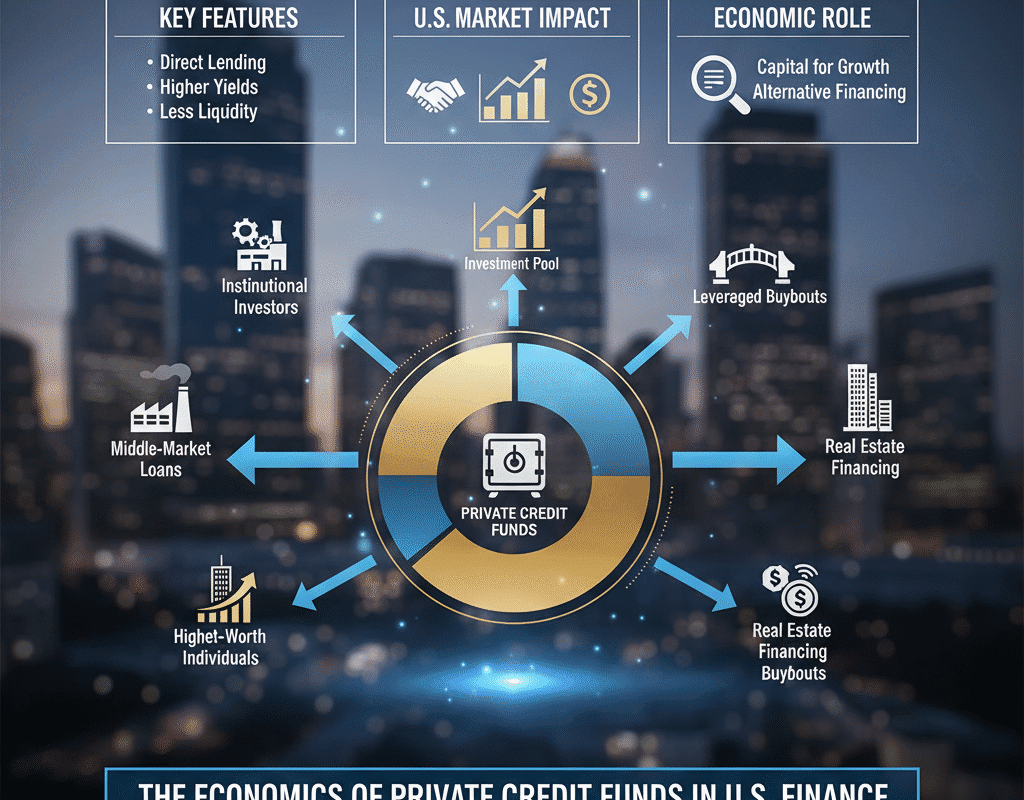

Private Credit Funds: What Are They?

Pooled investment vehicles known as private credit funds offer money to businesses directly, eschewing traditional banks. Private credit investments are usually illiquid, with longer-term commitments and negotiated lending terms, in contrast to public debt instruments that are traded on exchanges. These funds might focus on different kinds of lending, such as:

- Senior debt: Loans that, in the event of bankruptcy, take precedence over other obligations.

- Mezzanine finance is a type of hybrid debt that has equity-like characteristics like options or warrants.

- Distressed debt: Investments in companies facing financial distress but with potential for turnaround.

These funds cater primarily to mid-market companies that may not have access to public markets or traditional bank financing.

The Growth of Private Credit in the U.S.

Over the past decade, private credit has grown from a niche investment class into a multi-trillion-dollar market.

According to Preqin, private debt assets under management in North America surpassed $1 trillion in 2023, a figure that has been steadily rising due to regulatory changes, market volatility, and investor demand for yield. Several factors have fueled this growth:

- Banking regulations: Post-2008 financial crisis reforms, such as the Dodd-Frank Act, have constrained traditional banks from making certain types of loans, creating opportunities for non-bank lenders.

- Low-interest-rate environment: With conventional fixed-income yields at historic lows, institutional investors have sought higher returns from private credit.

Private Credit Funds’ Effect on the Economy

The American economy is impacted by private credit funds in a number of ways:

- Corporate growth: By financing mid-market companies that might struggle to access bank loans, private credit funds enable expansion, job creation, and innovation.

- Market competition: Non-bank lenders challenge traditional banking institutions, forcing them to adapt and improve lending practices.

- Financial stability: While offering alternative funding, these funds also concentrate risk among institutional investors, raising questions about systemic exposure in case of widespread defaults.

Concerns About Risk

Private credit funds have substantial dangers despite their alluring yields:

- Illiquidity risk: Investors may face difficulties redeeming capital before the end of the fund’s life cycle.

- Credit risk: Borrowers may default, particularly in high-yield or distressed lending strategies.

- Interest rate risk: Rising rates can affect borrowers’ ability to service debt, impacting fund returns.

To mitigate these risks, private credit fund managers conduct rigorous due diligence, including assessing company cash flows, collateral quality, and management capabilities.

Private Credit Investment Trends

Several notable trends are shaping the private credit landscape in the U.S.:

- Specialty lending: Funds targeting niche sectors such as healthcare, technology, and renewable energy are increasing.

- Direct lending: Bypassing intermediaries, funds provide loans directly to borrowers for growth, acquisition, or refinancing.

- Co-lending and club deals: Multiple funds collaborate to share large lending opportunities, spreading risk and enhancing returns.

- Sustainability-linked credit: ESG principles are increasingly incorporated into private credit deals, aligning investments with environmental and social goals.

In conclusion: The Economics of Private Credit Funds in U.S. Finance

Private credit funds have emerged as a powerful force in U.S. finance, offering alternative capital to companies and compelling returns to investors. By understanding the economics of these funds—including their structure, growth drivers, risks, and market impact—investors and policymakers alike can better navigate the evolving financial landscape.

As regulatory frameworks, market dynamics, and technological innovations continue to evolve, private credit funds are poised to play an even more significant role in shaping the future of corporate lending.

How State-Level Rainy Day Funds Impact Credit Ratings in the U.S.

How State-Level Rainy Day Funds Impact Credit Ratings in the U.S.