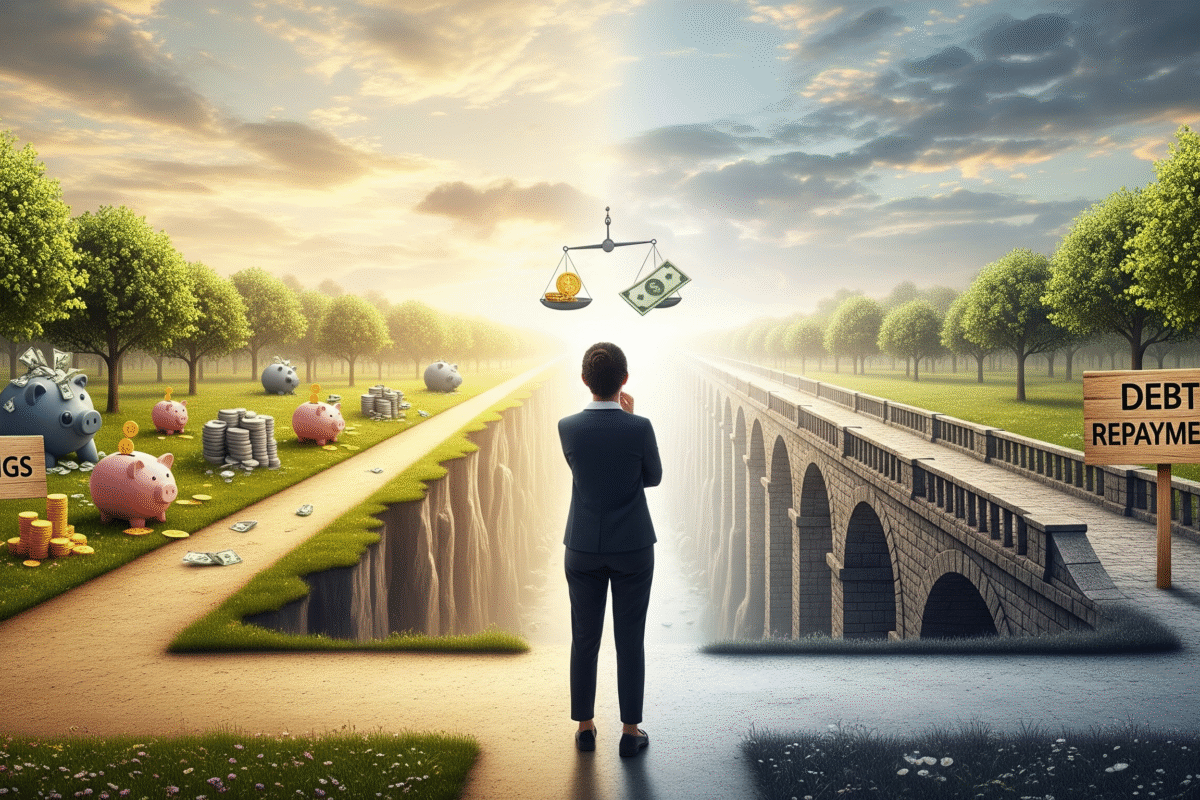

Should You Pay Off Debt or Save First?

Should You Pay Off Debt or Save First: A Common Dilemma in American Households

Millions of Americans struggle with the same urgent financial dilemma: should I prioritize saving money or paying off my debt?

It’s not an easy choice. With credit card interest rates averaging over 20% in 2025 and reports showing that 61% of Americans cannot cover a $1,000 emergency, the debate between debt repayment and savings is more relevant than ever.

Financial experts, consumer advocates, and everyday families are weighing in on this issue. Let’s break down what the latest research, expert opinions, and real-world case studies reveal about which path makes the most sense—and why the answer might not be the same for everyone.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

The Growing Debt Burden in the U.S.

According to the Federal Reserve, household debt in the United States has reached historic highs, surpassing $17 trillion in 2025. The breakdown includes:

- Credit card debt: Over $1.1 trillion, with record-high delinquency rates.

- Student loans: About $1.6 trillion remains outstanding.

- Auto loans: Nearly $1.6 trillion, with longer repayment terms than ever.

- Mortgage debt: Still the largest category, exceeding $12 trillion.

With rising interest rates, Americans are paying more in monthly minimums than in decades past. Yet at the same time, inflation has squeezed savings, making it harder to set money aside for emergencies or retirement.

This tug-of-war between debt repayment and savings has become one of the most crucial financial planning debates of our time.

The Argument in Favor of Debt Reduction First

High-interest debt, according to financial counselor and best-selling author David Bach of The Automatic Millionaire, is “a wealth killer.”

Experts advise paying off debt before making significant savings for the following key reasons:

Elevated Interest Rates surpass the returns on investments

Average yearly stock market return: 7–10% Average credit card annual percentage rate: 20%+

Debt repayment frequently yields a guaranteed return higher than that of most investments.

Relief of the Mind

People feel less stressed and more at ease when they pay off their debt. According to National Bureau of Economic Research studies, paying off debt enhances mental well-being.

Increasing Cash Flow

Every debt paid off reduces monthly commitments, freeing up funds that can subsequently be used for investments or savings.

How to Prevent a Debt Spiral?

Carrying balances puts people in a vicious circle of dependency by causing emergencies to swiftly result in increased borrowing.

- The Argument in Favor of Saving First

- On the other hand, many financial planners argue that building savings before aggressively paying down debt is the smarter long-term move.

- This is the reason:

- Emergency Fund Protection

- Without at least $500–$1,000 in savings, any small emergency (car repair, medical bill) can push people further into debt.

- Employer 401(k) Match

- Skipping employer-matching contributions means leaving free money on the table. Even while carrying debt, investing enough to capture a full match is often wise.

- Financial Security

- Savings provide a buffer against job loss or unexpected bills. The Consumer Financial Protection Bureau (CFPB) notes that families with even a few hundred dollars in savings recover from financial shocks faster.

- Debt Can Be Managed

- Not all debt is urgent. For example, low-interest federal student loans or mortgages may not require immediate payoff compared to building a strong savings foundation.

Considerations:

The best course of action is largely dependent on the particular situation. Important elements consist of:

Interest Rates: Prioritizing high-interest credit card debt is nearly always a good idea.

Job Stability: Having liquid savings may be more advantageous for people whose income fluctuates.

Mental Health: While some people feel safer with cash in the bank, others sleep better knowing they have no debt.

Retirement Plans: Tax-advantaged accounts and employer matching can help tip the scales in favor of saving.

Actual Situations

- The Credit Card Juggle Case Study

At 22% interest, Sarah, 32, has $8,000 in credit card debt.

She had saved about five hundred dollars.

Experts advise her to aggressively address her high-interest debt after increasing her emergency fund to $1,000.

- The Steady Professional Case Study

James, 40, is paying 4% interest on a $200,000 mortgage.

Contributions to his 401(k) are matched by his employer.

Financial advisors advise making enough contributions in this case to receive the entire 401(k) match, followed by further mortgage payments.

- The Family Provider Case Study

The parents of two, Maria and Luis, have $25,000 in student loan debt with 5% interest.

They have saved up two thousand dollars.

A hybrid strategy works best: continue minimum student loan payments while growing a larger emergency fund.

The Hybrid Approach: Balance Debt Repayment and Savings

Most financial advisors agree that a hybrid approach—balancing both debt payoff and savings—is the most sustainable strategy.

Steps in a Hybrid Strategy:

- Build a starter emergency fund of $1,000.

- Pay down high-interest debt (credit cards, payday loans).

- Contribute to retirement accounts at least up to the employer match.

- Grow savings to cover 3–6 months of expenses.

- Aggressively eliminate remaining debts.

This method prevents financial emergencies from derailing progress while steadily reducing debt burdens.

Newsworthy USA Trends in 2025

Recent surveys highlight shifting attitudes:

- Bankrate Survey 2025: 58% of Americans prioritize savings over debt repayment due to recession fears.

- Federal Reserve Data: Younger generations (Gen Z, Millennials) are more likely to build savings while carrying debt.

- Expert Debate: Economists warn that failing to address high-interest debt could trigger widespread financial instability.

This ongoing debate is shaping financial advice across media platforms, from TikTok influencers to Wall Street analysts.

Policy Viewpoint: How Government Activities Affect the Choice?

Whether or whether people should prioritize debt or savings is also influenced by government policies.

Student Loan Forgiveness Programs: Modifications in 2025 might relieve millions of people’s financial difficulties and put more emphasis on saving money.

Interest Rate Hikes: Higher borrowing costs make debt repayment more urgent.

Emergency Savings Incentives: Some employers are now offering payroll-linked savings accounts to encourage workers to save while still managing debt.

Expert Quotes to Note

- “If your debt is costing you more than you could reasonably earn by saving or investing, pay off the debt first.” — Mark Cuban, billionaire investor.

- “A small emergency fund is your first defense. Without it, debt will just keep piling up.” — Liz Weston, personal finance columnist.

- “Financial freedom isn’t about choosing debt OR savings. It’s about creating a system that balances both.” — Ramit Sethi.

In conclusion, what ought one to do?

- Depending on your financial status, interest rates, and risk tolerance, you can decide whether to pay off debt or save first.

- Create a small emergency fund and then quickly pay down any high-interest debt you may have.

- Make retirement contributions and savings your top priorities if your debt is modest and low-interest.

- For most Americans, a balanced hybrid approach—saving enough for emergencies while steadily reducing debt—is the smartest strategy.

Last Word

As financial challenges continue to rise in the U.S., the debate over debt versus savings will only intensify. What matters most is creating a personal plan that balances security today with financial freedom tomorrow.

How to Live Debt-Free in America?: Practical Tips for Financial Freedom

How to Live Debt-Free in America: Practical Tips for Financial Freedom