How Neobanks Are Competing with Traditional Banks?

How Neobanks Are Competing with Traditional Banks?

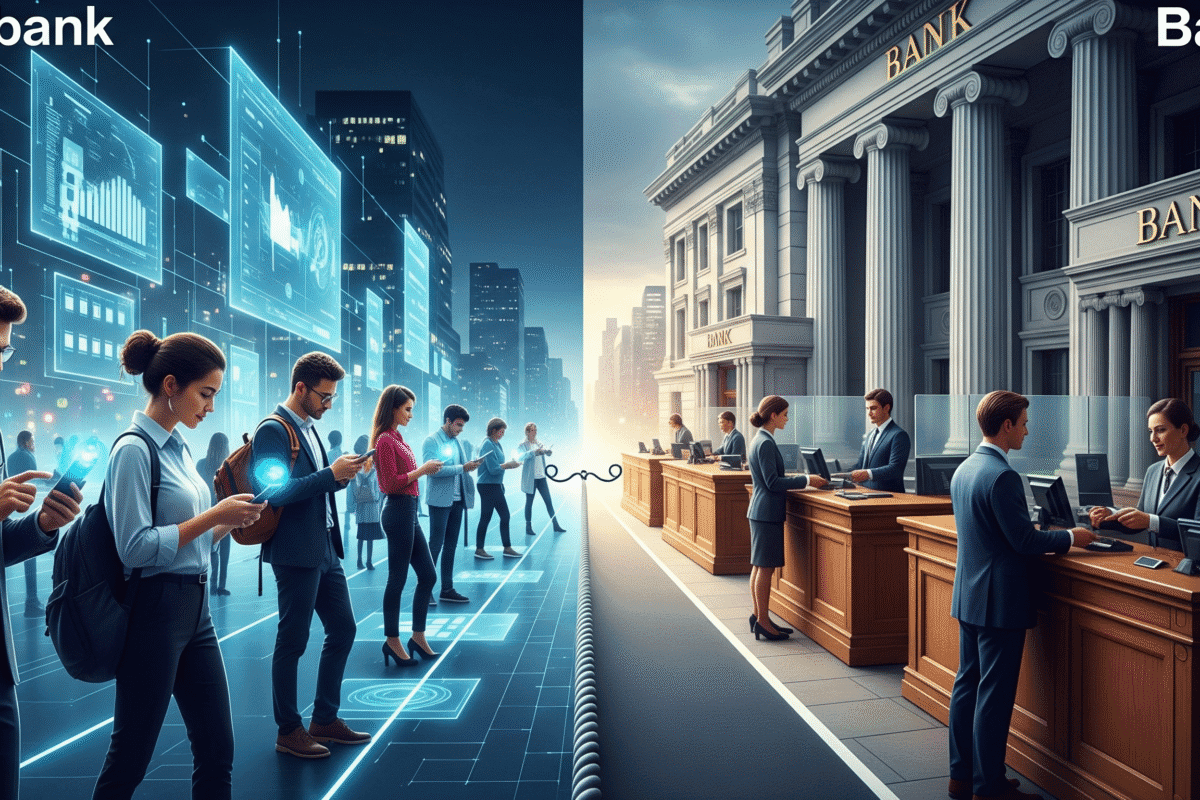

The banking sector is going through a dramatic change both domestically and internationally. For more than a century, traditional banks held the monopoly on financial services, offering savings accounts, loans, credit cards, and mortgages through physical branches. However, the rise of neobanks—also known as challenger banks—has dramatically altered the competitive landscape.

Unlike traditional banks, neobanks operate exclusively online, without costly branch networks, and focus heavily on user experience, digital-first services, and low fees. With millions of Americans turning to mobile apps for everything from food delivery to investment management, neobanks are gaining momentum and positioning themselves as strong competitors to legacy institutions.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

What Are Neobanks?

Neobanks are digital-only banks that operate primarily through mobile apps and web platforms. Unlike traditional banks, they typically do not hold a full banking license but partner with licensed financial institutions to provide FDIC-insured services.

Some well-known neobanks in the U.S. include:

- Chime

- Varo Bank

- Current

- Revolut (U.S. operations)

- SoFi (though more hybrid fintech-bank)

Neobanks offer services such as:

- Checking and savings accounts

- Debit and prepaid cards

- Instant peer-to-peer transfers

- Early access to paychecks

- Budgeting tools and AI-powered insights

Their primary appeal lies in simplicity, low cost, and mobile-first convenience.

Traditional Banks: Advantages and Disadvantages

The financial industry is still dominated by traditional banks, which hold most of the assets and provide a wide range of services like business loans, investment accounts, and mortgages. Nevertheless, they also have flaws in addition to their strengths:

Traditional Banks’ Advantages

- Developed brand awareness and trust

- broad range of products (from mortgages to credit)

- Physical locations for on-site support

- robust regulatory support

Traditional Banks’ Drawbacks

- Increased costs (maintenance, overdraft, and ATM fees)

- Innovation cycles that are slower because of old infrastructure

- A less customized experience for customers

- Branch-focused, which restricts younger, mobile-first consumers’ access

How Neobanks Face Off Against Conventional Banks

- Banking without fees

Fees are among the main complaints from clients. Overdrafts, minimum balance requirements, and overseas transactions are all subject to fees at traditional banks. Neobanks upends this paradigm by providing:

- No maintenance costs per month

- No overdraft charges, up to a certain amount

- Use of foreign cards is free.

For example, Chime attracts millions of cost-conscious consumers by marketing itself as a “fee-free banking alternative.”

- User Experience with a Digital Focus

Apps, not branches, form the foundation of Neobanks. They have slick, user-friendly, and customizable interfaces. Clients can:

- Create an account in a matter of minutes.

- Track spending instantly

- Make use of AI-powered financial resources

- Use chat to get 24/7 customer service.

Millennials and Gen Z, who are less likely to visit physical branches, are particularly drawn to this digital ease.

- Quicker Services and Early Paycheck Access

While traditional banks take 1–3 days to clear direct deposits, many neobanks offer early paycheck access, giving users funds up to two days sooner. This feature has been especially attractive for gig economy workers and employees living paycheck to paycheck.

- Targeting Underserved Markets

Neobanks are addressing segments often overlooked by traditional banks, such as:

- Unbanked and underbanked individuals

- Gig economy workers without stable income

- Small businesses and freelancers seeking flexible tools

By eliminating credit history requirements for basic accounts and offering low-cost services, neobanks provide financial inclusion at scale.

- Cross-Border Services and Global Reach

Neobanks provide worldwide usability, in contrast to many traditional banks that are dependent on regional infrastructure. For instance, Revolut enables users to use cards anywhere in the globe, hold different currencies, and send international payments at reduced costs.

- Personal Finance & Budgeting Tools

Neobanks integrate AI-driven insights and budgeting tools directly into their apps, helping users track spending, categorize expenses, and save automatically. Traditional banks often require third-party apps for similar functionality.

- Integration with Fintech Ecosystems

Challenger banks often partner with fintech services like PayPal, Venmo, Cash App, and investment platforms. This interconnectedness creates a one-stop financial ecosystem that appeals to tech-savvy users.

Challenges Neobanks Face

While neobanks are growing rapidly, they also face hurdles:

- Lack of Full Banking Licenses – Many rely on partnerships with traditional banks for FDIC insurance.

- Trust Issues – Older generations still prefer institutions with long histories.

- Limited Services – Most neobanks do not yet offer mortgages, large-scale loans, or wealth management.

- Profitability Concerns – Operating on low fees means they need large customer bases to generate revenue.

- Regulatory Scrutiny – As neobanks grow, regulators are watching closely to prevent risks to consumers.

Conventional Banks Retaliate

Conventional banks are not doing nothing. In response to neobank competition, they are:

- Investing heavily in digital transformation (e.g., JPMorgan Chase mobile app).

- Launching their own digital-first subsidiaries (e.g., Goldman Sachs’ Marcus).

- Partnering with fintech startups to stay competitive.

- Cutting certain fees to match neobank offerings.

By leveraging their size and trust, traditional banks aim to blend legacy reliability with digital convenience.

The Future of Banking: Collaboration or Competition?

Industry experts suggest the future may not be purely competitive. Instead, collaboration between neobanks and traditional banks could dominate.

- Neobanks bring agility, user experience, and digital innovation.

- Traditional banks bring trust, licenses, and comprehensive financial services.

The convergence of these strengths could redefine the banking landscape.

2025 Consumer Attitudes

In 2025, recent surveys show:

- 42% of U.S. Millennials now have at least one neobank account.

- 65% of Gen Z consumers prefer mobile-only banking over physical branches.

Traditional banks still dominate in mortgages and business loans, but neobanks are gaining ground in everyday banking needs.

In Conclusion

The battle between neobanks and traditional banks is reshaping the financial industry in 2025. Neobanks are winning customers with digital-first experiences, low fees, and financial inclusivity, while traditional banks leverage scale, trust, and regulatory power.

In the coming years, the lines between them may blur as traditional banks adopt more digital tools and neobanks expand into broader financial services. For consumers, this competition means better banking experiences, lower costs, and more innovation.

Top Financial Mistakes Small Business Owners Make and How to Avoid Them

Top Financial Mistakes Small Business Owners Make and How to Avoid Them