How 401(k) Contributions Reduce Taxable Income?

How 401(k) Contributions Reduce Taxable Income?

As the 2025 tax season approaches, millions of American workers are looking for ways to reduce their taxable income legally and efficiently. One of the most powerful and IRS-approved methods is contributing to a 401(k) retirement plan.

A 401(k) is not just a savings tool for your future—it’s also a strategic tax shield that can lower how much of your income the government taxes each year. In this article, we’ll break down exactly how 401(k) contributions reduce taxable income, the 2025 limits, the difference between traditional and Roth 401(k) accounts, and practical examples of how much you can save.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

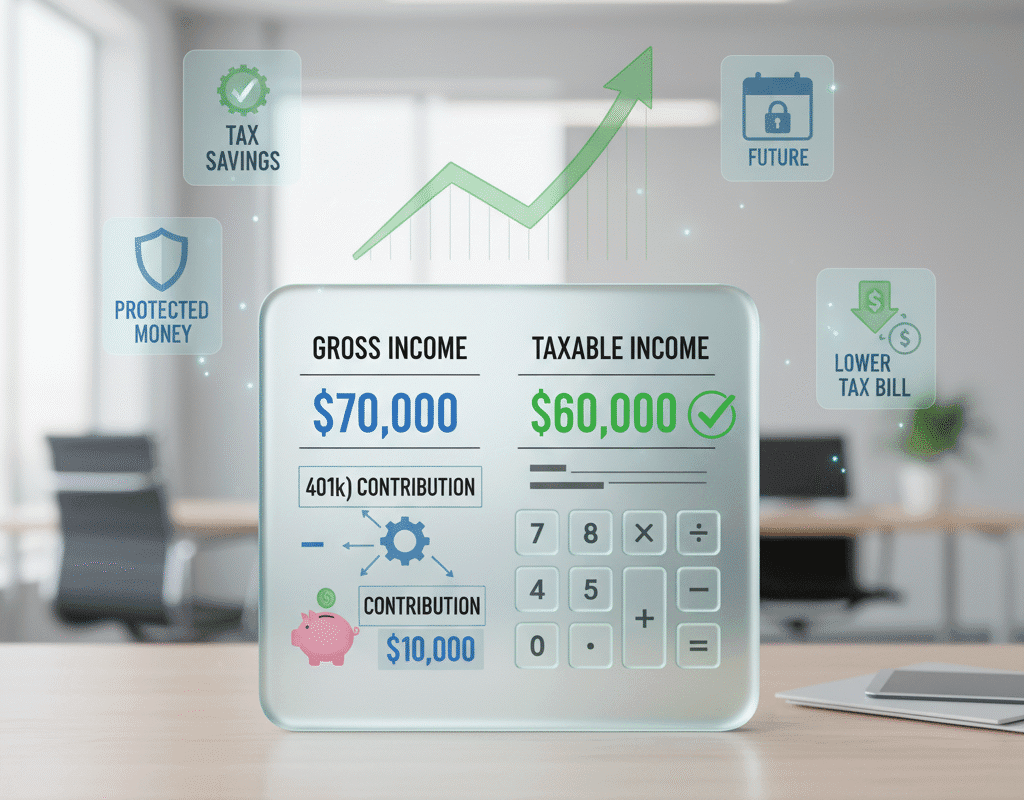

What Is a 401(k) and How Does It Work?

A 401(k) plan is a tax-advantaged retirement savings account offered by many U.S. employers. Employees can elect to have a portion of their paycheck automatically deposited into their 401(k) account before taxes are applied.

These contributions grow tax-deferred, meaning you don’t pay taxes on the money you contribute

401(k) Contribution Limits

or its investment growth until you withdraw it—usually after age 59½.

Key Components of a 401(k):

- Employee Contributions: The amount you choose to set aside from each paycheck.

- Employer Match: Many companies match part of your contribution, offering “free money” for retirement.

- Tax Advantages: Contributions reduce your taxable income for the year.

401(k) Contribution Limits for 2025

According to the IRS, contribution limits are adjusted annually for inflation. For tax year 2025, the limits are as follows:

| Type of Contribution | 2025 Limit |

| Employee Elective Deferral | $23,000 |

| Catch-Up Contribution (Age 50+) | $7,500 |

| Combined Total (Employee + Employer) | $69,000 or $76,500 (50+) |

These limits mean that individuals under 50 can contribute up to $23,000 of pre-tax income, directly reducing their taxable earnings for the year.

Employer Match: A Bonus Free of Taxes

A 401(k) match, usually between 3% and 6% of your pay, is offered by many American businesses.

For instance, you may get $3,500 in free retirement contributions annually if your company matches 5% of your $70,000 salary.

This game:

- Is not included in your taxable income.

- Increases tax-deferred

- Effectively raises your pay without adding to your tax liability

The Long-Term Benefit: Compound Growth, Tax-Deferred

When you invest in a 401(k), your earnings—dividends, capital gains, and interest—grow tax-deferred.

That means you don’t pay taxes each year as your account grows, allowing your balance to compound faster.

Example:

- Invest $10,000 yearly for 25 years

- Average return: 7%

- Without taxes (401k): Grows to $656,000

- With annual taxes (non-retirement): Grows to $490,000

That’s a $166,000 advantage—thanks purely to the tax-deferred structure.

Strategic Advice to Get the Most Out of Your 401(k) Tax Benefits

- Make Early and Regular Contributions

Your money compounds tax-deferred for a longer period of time the earlier you start.

- Attend the Employer Match

Contributions should always be sufficient to receive the full match, which is tax-free money.

- Make Use of Catch-Up Contributions (Over 50)

Use the additional $7,500 cap to further reduce your taxes if you are 50 years of age or older.

- Modify Contributions in Light of Raises

To prevent lifestyle inflation, increase your contribution percentage each time your pay rises.

- Coordinate with Additional Tax Deductions

You may be eligible for additional credits, such as the Child Tax Credit or Education Credits, if you lower your AGI through a 401(k).

Comparing IRA and 401(k) Savings

IRAs and 401(k)s both have tax advantages, but 401(k)s allow significantly larger contributions and frequently include company matching.

| Feature | 401(k) | IRA |

| Annual Limit (2025) | $23,000 | $7,000 |

| Employer Match | Yes | No |

| Pre-Tax Contributions | Yes | Yes (Traditional IRA) |

| Roth Option | Yes | Yes |

| Accessibility | Through Employer | Individually Opened |

The Trade-Off: Later Tax Payment

When you take money out of your regular 401(k) in retirement, taxes are eventually collected by the IRS.

However, withdrawals are frequently taxed at a reduced rate because the majority of people have lower taxable income in retirement.

For instance:

- 24% is the working tax rate.

- 12% is the retirement tax rate.

You made a wise tax decision by saving 24% up front and paying 12% later.

401(k) Tax Planning Strategies for 2025

- Front-load contributions early in the year to maximize growth.

- Consider Roth conversions during low-income years.

- Coordinate with Health Savings Accounts (HSAs) for extra pre-tax savings.

- Optimize for your tax bracket — avoid contributing so much that you drop into an unusually low bracket and lose other deductions.

- Rebalance investments annually for risk management and long-term growth.

Concluding Remarks: The Significance of 401(k) Contributions in 2025

Making the most of your 401(k) involves more than just retirement because of inflation, growing living expenses, and Social Security uncertainty. It also involves tax efficiency and financial control.

For each $1 you donate:

- Lowers your present taxable income.

- Increases wealth in the future

- Employer matching may be available. Compounds are tax-deferred for many years.

One of the best financial decisions any American worker can make in 2025 is to contribute to their 401(k), which will help them save money both now and in the future.

In conclusion: How 401(k) Contributions Reduce Taxable Income?

Making contributions to your 401(k) is an instant tax strategy that puts money back into your pocket, not just a retirement plan.

You may optimize your short-term savings and long-term financial independence by lowering your taxable income, taking advantage of employer matches, and allowing your savings to grow tax-deferred.

As 2025 unfolds, financial planners continue to recommend maximizing 401(k) contributions as one of the most effective ways to reduce taxable income in America.

How FICO Scores Are Different from VantageScores: What Every Borrower Should Know

How FICO Scores Are Different from VantageScores: What Every Borrower Should Know