Dollar-Cost Averaging vs Lump-Sum Investing:

Dollar-Cost Averaging vs Lump-Sum Investing: Overview

In the world of personal finance, one enduring question continues to spark debate: Should you invest a windfall all at once or spread it over time? This dilemma lies at the heart of two key strategies—lump-sum investing and dollar-cost averaging (DCA).

As investors navigate volatile markets, rising interest rates, and uncertain global economics, weighing the emotional and financial implications of each approach is vital. This article examines the latest research, expert opinions, and real-world scenarios to help you decide which method aligns best with your goals and temperament.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

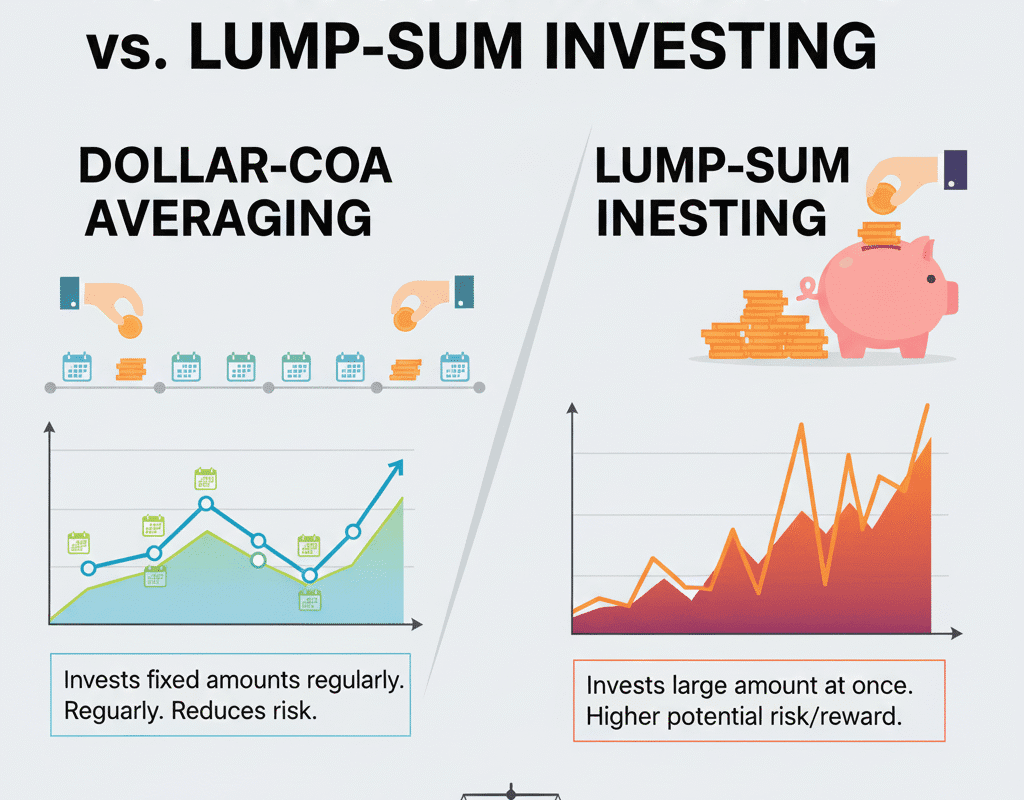

Dollar-Cost Averaging (DCA): What Is It?

Dollar-Cost Averaging is an investment strategy where you invest a fixed amount of money at regular intervals—monthly, quarterly, or annually—regardless of market conditions.

For example, instead of investing $12,000 all at once, you could invest $1,000 each month for 12 months. This way, you purchase more shares when prices are low and fewer shares when prices are high, potentially lowering your average cost per share over time.

The advantages of averaging costs in dollars

- Reduces Emotional Bias – Investors don’t need to time the market, which reduces stress and decision-making errors.

- Reduces Risk: You can avoid the danger of making all of your investments right before a market meltdown by spreading out your purchases.

- A disciplined approach promotes regular investment practices, which are perfect for retirement savings and long-term asset accumulation.

- Better for Volatile Markets: This strategy performs well in markets with large price swings.

Drawbacks of Dollar-Cost Averaging

- Potentially lesser Returns Compared to lump-sum investing, waiting full investment may yield lesser returns if markets are typically trending upward.

- Opportunity Cost: Capital that is left on the sidelines does not increase as quickly as capital that is invested.

- Not the best option for sizable bonuses or inheritances because uninvested large sums of money may lose their purchasing power.

Lump-sum investing: what is it?

One-Sum When you invest, you put all of your money into the market at once rather than distributing it over time. For instance, investing $12,000 all at once as opposed to breaking it up into monthly payments.

Advantages of Investing in Large Sums

- Optimizes Market Exposure: Capital immediately begins compounding, capitalizing on long-term growth patterns.

- Higher Returns in the Past: Research indicates that markets tend to rise more frequently than fall, thus investing completely typically yields favorable results.

- Simple Strategy: One-time choice, no continuous supervision.

Drawbacks of Lump-Sum Investing

High Risk of Poor Timing – If markets drop right after you invest, your portfolio could take a big hit.

- Psychological Stress – Investors may feel regret if they enter the market just before a downturn.

- Requires Strong Risk Tolerance – Not suitable for investors who panic during volatility.

Historical Information: Which Is Better?

- Lump-Sum investing performs better than Dollar-Cost averaging almost two-thirds of the time, according to a number of studies, including those conducted by Vanguard and Morningstar. This is due to the long-term tendency of markets to rise.

- Historical S&P 500 data: Generally speaking, investors who make lump sum investments enjoy higher average returns over a 10-year period than those who make progressive investments.

- Exceptions: Dollar-Cost Averaging offers superior protection against large declines or recessions.

Effects on Investors’ Minds

Investing involves more than simply math; it also involves feelings. Many investors are reluctant to risk all of their money at once because they are afraid of market downturns.

- Cost in dollars By lowering anxiety, averaging makes it simpler for cautious investors to begin investing.

- One-Sum Discipline, patience, and the capacity to overlook transient volatility are necessary for investing.

Real-Life Example: $100,000 Investment

Lump-Sum Investing

- Invested immediately in the S&P 500 at the start of 2015.

- By the end of 2024, it grew to approximately $300,000.

Dollar-Cost Averaging

- Invested $10,000 annually from 2015–2024.

- Ended up with around $250,000.

Result: Lump-Sum Investing won in a rising market.

But if markets had crashed early in the period, DCA could have provided better protection.

Who Should Use Dollar-Cost Averaging?

- New investors nervous about volatility

- People with regular income streams (salary earners contributing to 401(k) or IRA)

- Risk-averse investors

- Long-term planners who value consistency

Who Should Use Lump-Sum Investing?

- Experienced investors comfortable with market risk

- People receiving large sums of money (inheritance, bonus, asset sale)

- Investors with long time horizons (10+ years)

- Those seeking maximum compounding potential

Conclusion: Which Strategy Should You Choose?

The debate between Dollar-Cost Averaging vs Lump-Sum Investing will continue as long as markets exist. Historically, Lump-Sum Investing has delivered higher returns in most scenarios, but Dollar-Cost Averaging provides peace of mind and risk reduction during volatile times.

The best choice depends on your personality, financial situation, and long-term goals. If you can handle market swings, Lump-Sum Investing may maximize growth. If you value stability and steady progress, Dollar-Cost Averaging is your friend.

In 2025, as global uncertainty lingers, many investors may prefer a hybrid approach—part lump sum, part gradual investing—to balance returns with risk management.

Life Insurance: Term vs Whole Life Explained | Benefits, Costs, and Which is Best

Life Insurance: Term vs Whole Life Explained | Benefits, Costs, and Which is Best