The Impact of Rising Mortgage Rates:

The Impact of Rising Mortgage Rates:

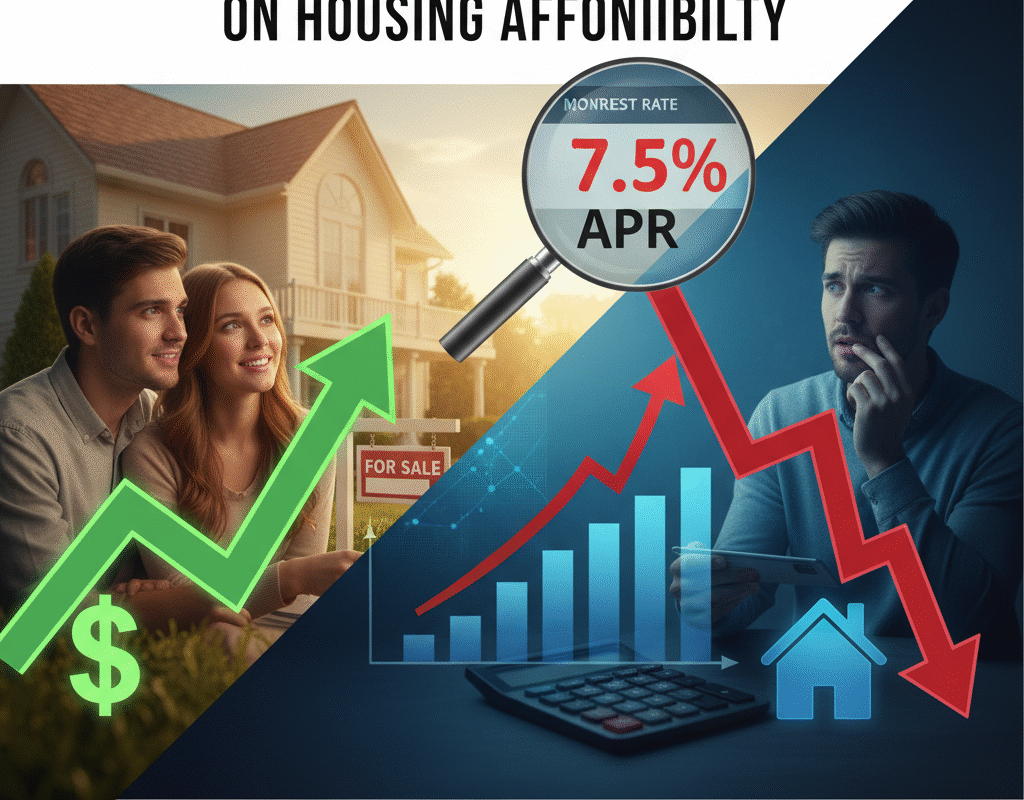

One of the most important factors in the process, mortgage interest rates, is posing a growing threat to the American goal of homeownership. Rising interest rates diminish borrowing power, increase monthly payments, impede mobility, and intensify constraints on affordability. The current situation has changed for both homeowners and potential homebuyers due to the combination of high housing prices and high mortgage rates.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

The Current Rate Environment & How We Got Here

Mortgage rates in the U.S. have surged from the historically low levels seen during the pandemic. According to the Consumer Financial Protection Bureau (CFPB), the average rate on a 30-year fixed mortgage rose from around 2.65 % in January 2021 to a peak of nearly 7.79 % in October 2023.

The increase was driven by several factors: the rapid inflation of the post-pandemic period, aggressive rate hikes by the Federal Reserve, a withdrawal of liquidity from mortgage-backed securities markets, and a widening spread between Treasury yields and mortgage rates.

While rates have eased somewhat, they remain at historically high levels compared to the ultra-low era of 2020-21. The outcome: higher borrowing costs and a reshaped affordability landscape.

Limitations on Supply Boost the Issue

The availability of homes influences affordability in addition to mortgage rates and pricing. The effects of high rates are intensified by a limited supply.

Development and Construction Lag

Due to high capital expenditures, high material costs, labor shortages, and regulatory restrictions, development activity has halted. According to a CBRE Investment Management report, new house sales fell precipitously and turnover was considerably decreased by increasing mortgage rates.

Land-use and Regulatory Barriers

According to Goldman Sachs analysis, the United States needs to build an extra 3–4 million homes over current building levels—roughly 2-2.6% of the present housing stock—in order to restore affordability. Zoning and restricted land-use regulations are the largest obstacles.

Variation by Region and Market

The effects of mortgage rates vary by region in the United States. Areas with higher home-price multiples, such areas of the West and Northeast, are more affected in terms of affordability. In states with robust job growth and housing supply limits, monetary policy changes also typically have greater effects on housing prices.

The rate hike still reduces borrowing capacity and drives out marginal purchasers in areas where prices are lower but earnings are also lower. Rising rates worsen already narrow affordability bands in high-cost economies.

What Takes Place Next? Prospects and Policy Issues

The trajectory of mortgage rates

The speed at which mortgage rates move will be important: more rate increases would make borrowing more difficult; rate decreases would offer some respite, but they wouldn’t bring back the extremely low interest rates of the epidemic era. The payment on a median-priced property remained about 52% higher than during the low-rate era, according to the CFPB, despite rates relaxing to about 6.20% in September 2024.

Prospects for Home Prices

In certain markets, price growth may halt or even reverse if high rates continue to limit demand. However, if supply is still limited, prices can stay high. According to research, since mid-2022, rate rises have emerged as the primary cause of decreased affordability.

Building More Homes

Long-term affordability hinges on increasing housing supply. Goldman Sachs estimates around 3-4 million additional units are needed to restore historical price-to-income norms.

Alternative Financing & Policy Responses

Some proposals include longer-term mortgages (e.g., 50-year terms), assumable loans, or special programs for first-time buyers. However, experts caution that extending terms may lower monthly payments but increase total interest costs and may fuel higher prices if supply remains constrained.

The Impact of Inflation and Income Growth

Growth in income also affects affordability. Elevated rates and prices are somewhat countered if wages increase more quickly than housing costs. But if income gains stall — as recent data suggest in some segments — affordability remains under stress.

In conclusion: The Impact of Rising Mortgage Rates

The home affordability environment in the United States has undergone significant changes due to rising mortgage rates.

For many purchasers, what was previously a tolerable additional expense is now a significant obstacle. Important lessons learned:

- High mortgage rates drastically lower borrowing power and increase monthly payments.

- Affordability has been severely constrained by the combination of high rates and high property prices.

- The issue is exacerbated by supply limits, which are partly caused by homeowners who are tied into low rates and regulatory obstacles to new building.

- The impact varies by buyer type, income level, and geographic location, but generally speaking, many people now have fewer options for becoming homeowners.

- Relief might only materialize gradually, either through significant increases in the supply of homes, higher wage growth, or rate reductions.

For anyone navigating the housing market today, the message is clear: interest-rate risk matters now more than ever. Being well-informed, realistic about budgets, and strategic about timing and location may make the difference between securing a home versus being priced out.

Why Some U.S. States Face Budget Crises: Causes, Trends & Risks

Why Some U.S. States Face Budget Crises: Causes, Trends & Risks