The Role of Freddie Mac and Fannie Mae:

The Role of Freddie Mac and Fannie Mae:

Two of the most significant organizations in the US housing finance sector are Freddie Mac and Fannie Mae. Officially referred to as government-sponsored enterprises (GSEs), they are essential to maintaining the mortgage market’s affordability, stability, and liquidity. For millions of American families, getting a house loan would be much more difficult and costly without them.

Freddie Mac and Fannie Mae are still as relevant as ever as the U.S. housing market changes due to shifting interest rates, inflationary pressures, and policy changes. Knowing their roles, responsibilities, and difficulties helps us understand how Americans maintain their desire of homeownership despite economic uncertainties.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

Freddie Mac and Fannie Mae’s History

1.1 Fannie Mae’s Creation

The Federal National Mortgage Association (Fannie Mae) was established in 1938 during the Great Depression as part of President Franklin D. Roosevelt’s New Deal. Its main goal was to revive the housing market by creating a secondary mortgage market. Before Fannie Mae, local banks could only lend based on their own deposits. Once those funds ran out, lending stopped—restricting homeownership opportunities.

Fannie Mae changed that. By purchasing mortgages from lenders, it freed up their capital, allowing them to issue more home loans. This system created a continuous flow of money through the housing market, stimulating economic growth.

1.2 The Birth of Freddie Mac

The Federal Home Loan Mortgage Corporation (Freddie Mac) was founded later in 1970, primarily to compete with Fannie Mae and expand the secondary mortgage market. Freddie Mac provided additional liquidity and ensured that savings and loan institutions (thrifts) had a stable buyer for their mortgages.

Both institutions, though distinct, share the same purpose: to make mortgage credit more accessible and affordable for American borrowers.

The Functions of Fannie Mae and Freddie Mac

2.1 The Secondary Mortgage Market

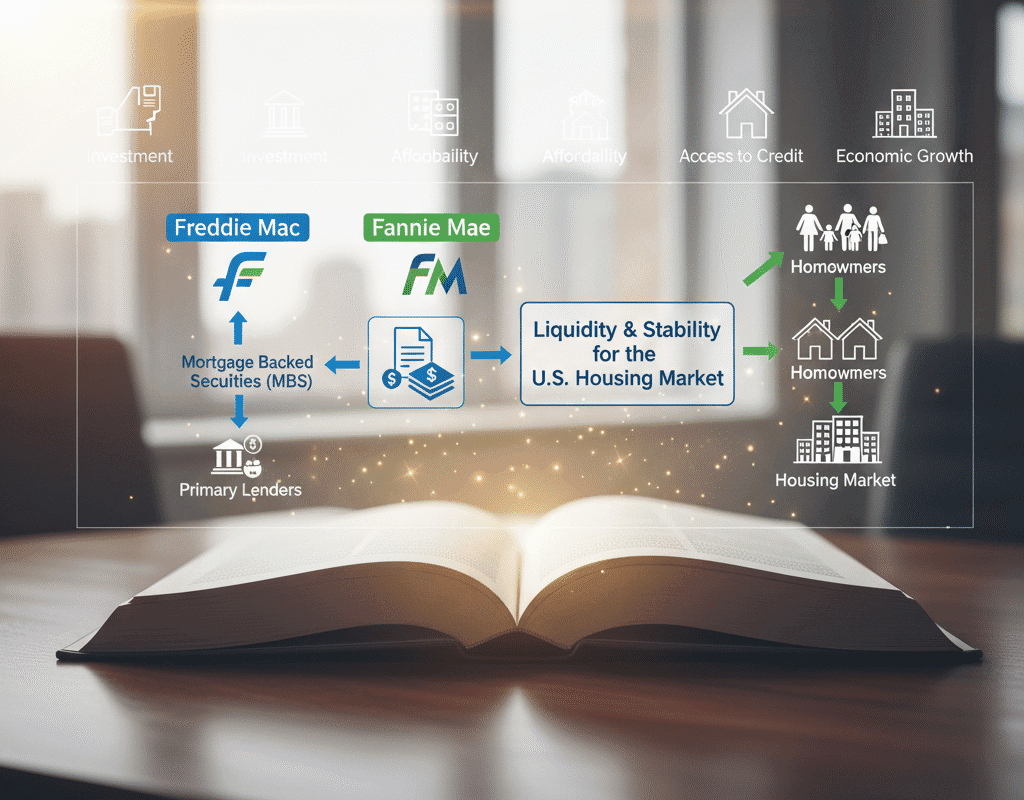

Homebuyers do not receive direct loans from Freddie Mac or Fannie Mae. Rather, they purchase mortgages from lenders and banks, bundle them into mortgage-backed securities (MBS), and then offer those to investors.

This procedure achieves a number of objectives:

- It gives lenders more money so they may give out more loans.

- It lowers local banks’ exposure to risk.

- It stabilizes mortgage interest rates across the country.

Essentially, the GSEs act as financial intermediaries between lenders and investors, ensuring a steady flow of funds through the housing finance system.

2.2 Guaranteeing Mortgage-Backed Securities

When Freddie Mac and Fannie Mae create MBS, they also guarantee the timely payment of principal and interest to investors. This guarantee, backed by the U.S. government’s implicit support, makes these securities highly attractive and low-risk investment options.

In turn, this lowers borrowing costs for homeowners and helps maintain market confidence—even during economic turbulence.

Freddie Mac and Fannie Mae’s Effect on the Housing Market

3.1 Making Homeownership More Accessible

Millions of Americans who otherwise could not afford homes are able to purchase them thanks to the GSEs’ stabilization of the mortgage market. Lenders are encouraged by their rules to provide 30-year fixed-rate mortgages, a distinctive

3.2 Maintaining Low Mortgage Rates

Interest rates remain lower than they could otherwise be because of the GSEs’ capacity to draw investors to mortgage-backed securities, which guarantees a consistent demand for home loans.

3.3 Endorsing Initiatives for Affordable Housing

Additionally, Freddie Mac and Fannie Mae are responsible for promoting affordable housing. They finance loans in underserved areas and reserve a portion of their portfolios for borrowers with low and moderate incomes.

Government Conservatorship and the 2008 Financial Crisis

4.1 The Emergence of the Crisis

The housing finance system’s weaknesses were exposed by the 2008 financial crisis. Risky subprime mortgages were a significant exposure for both GSEs. Defaults increased and the value of mortgage-backed securities fell as home prices fell.

Both Freddie Mac and Fannie Mae were in danger of going bankrupt by September 2008. The U.S. government stepped in to keep the housing market from completely collapsing.

4.2 FHFA Assumes Command

On September 6, 2008, Freddie Mac and Fannie Mae were placed under conservatorship by the Federal Housing Finance Agency (FHFA). This meant that in order to stabilize the institutions and regain market confidence, the government assumed management. To ensure that the GSEs could continue to function, the Treasury offered capital support in return for preferred shares.

The Federal Housing Finance Agency’s (FHFA) Function

The FHFA is in charge of overseeing and protecting Fannie Mae and Freddie Mac. Its goal is to guarantee that these organizations run solidly, safely, and in a way that supports the real estate market.

5.1 Capital and Oversight Needs

To make sure the GSEs can withstand possible losses, the FHFA sets capital requirements. Reforms after the crisis reduced taxpayer liability by requiring the GSEs to keep more capital in proportion to their risk exposure.

5.2 Objectives for Affordable Housing

Both Freddie Mac and Fannie Mae are required by the FHFA to reach yearly targets for affordable housing, with an emphasis on:

- Minority and low-income borrowers

- Communities that are not well served

- Development of multifamily dwellings

By doing this, it is guaranteed that the GSEs would continue to support equitable homeownership options.

The Current Role and Difficulties of Freddie Mac and Fannie Mae in 2025

6.1 Handling Uncertainty in the Economy

As of 2025, the U.S. housing market is confronted with challenges related to limited housing supply, affordability concerns, and shifting interest rates. Fannie Mae and Freddie Mac are essential to preserving stability in the face of these challenges.

Lenders and investors are reassured by their steady presence, which helps avoid the kind of credit tightening that can slow the economy.

6.2 Encouraging the affordability of housing

Both organizations have implemented cutting-edge initiatives to increase homeownership:

- Low down payment choices are available through Fannie Mae’s “HomeReady” and Freddie Mac’s “Home Possible.”

- Reducing the racial homeownership gap is the goal of special incentives for minority households and first-time purchasers.

The GSE Reform and Privatization Debate

7.1 The Reform Movement

Policymakers have been debating whether to privatize or reform Freddie Mac and Fannie Mae since the 2008 financial crisis. Government intervention, according to critics, distorts the market and exposes taxpayers to possible bailouts.

However, proponents claim that GSEs are necessary to preserve market liquidity and affordable homeownership.

7.2 Suggested Changes

A number of suggestions have been made:

- Reducing government assistance and enabling private companies to compete is known as full privatization.

- Utility Model: The GSEs continue to function as public utilities while being subject to regulation.

- Hybrid Models: Bringing together private investment and public supervision.

Freddie Mac and Fannie Mae’s Global Significance

In addition to having an impact on the American economy, Freddie Mac and Fannie Mae also have an impact on international financial markets. Their mortgage-backed securities are benchmarks for stability and draw in investors from all over the world.

By keeping interest rates competitive and strengthening the dollar, foreign demand for U.S. MBS connects U.S. housing finance to global capital flows.

Rebuttals and Disputations

9.1 Issues with Moral Hazard

One recurring criticism is that implicit government backing encourages moral hazard, where the GSEs may take excessive risks assuming taxpayer bailouts would follow in a crisis.

9.2 Market Distortion

Some analysts argue that Freddie Mac and Fannie Mae crowd out private competitors by dominating the secondary mortgage market. Without them, private investors might play a larger role in shaping housing finance.

In conclusion: The Role of Freddie Mac and Fannie Mae in the U.S.

The American housing finance system is still based on Freddie Mac and Fannie Mae. Since their inception, they have empowered millions of families to achieve homeownership and strengthened the overall economy through a stable, liquid mortgage market.

While debates over their reform continue, one fact is clear: the U.S. housing market cannot function effectively without them. As the country navigates 2025’s economic challenges—from affordability crises to global market shifts—these institutions will continue to evolve, adapting to ensure that the dream of homeownership remains within reach for all Americans.

Why States Issue Municipal Bonds: Understanding Purpose, Benefits, and Impact

Why States Issue Municipal Bonds: Understanding Purpose, Benefits, and Impact