Why Taxpayers Fund Public Retirement Systems?

Why Taxpayers Fund Public Retirement Systems?

In the United States, when we talk about retirement systems for public-sector workers, we inevitably confront the role of taxpayers. Why do taxpayers fund public retirement systems for government employees? What are the benefits, the costs, and the long-term implications?

This article explores the rationale behind taxpayer-funded public retirement systems, the ways in which they serve both workers and the public interest, the financial and demographic challenges they face, and the policy options that might improve their sustainability.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

What are public retirement systems?

Public retirement systems — also known as public employee pension systems — refer to retirement benefit frameworks provided to employees of governments (federal, state & local) in roles such as teachers, police officers, fire-fighters, other civil servants. These plans may be defined benefit (DB) plans, where a retiree receives a set benefit (often based on years of service, salary, and a multiplier), or defined contribution (DC) plans, where retirement income depends on contributions plus investment returns.

According to research from The Pew Charitable Trusts, although taxpayer contributions to state pension plans have nearly doubled as a share of state revenue over the past decade, many systems still face a more than $1 trillion shortfall.

How taxpayer funding works in practice

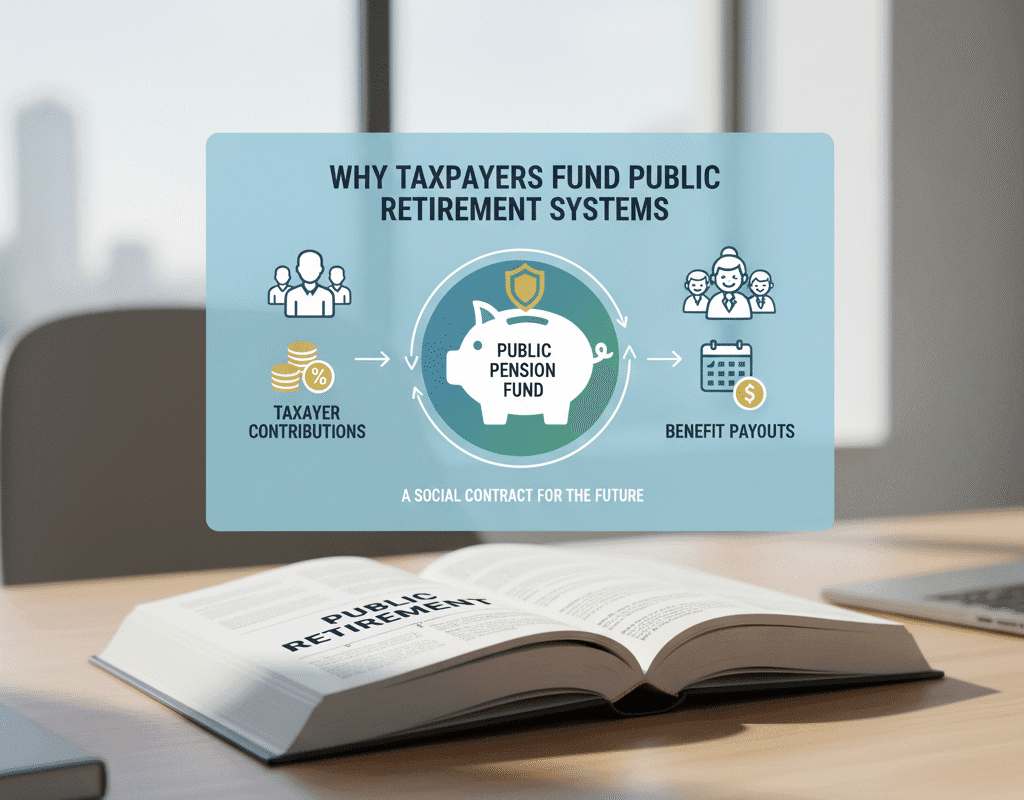

Public retirement systems are funded via several channels. These include employee contributions, employer (government) contributions, investment returns, and ultimately taxpayer revenues (either via general taxation or earmarked funds).

- Employee contributions: Many public-employee pension plans require workers to contribute a portion of their salary over their working years.

- Employer/Government contributions: The employing government entity often contributes a portion intended to cover the employer’s share of the retirement benefit cost.

- Investment returns: Pension funds invest the contributions to grow the asset base and reduce the required contributions from taxpayers. For example, investment returns in many state-local DB plans historically accounted for a large share of benefit payments.

The “why” condensed: Why the expense is borne by taxpayers

In summary, the main reasons why taxpayers support public retirement schemes are:

- Pensions assist governments in attracting and retaining a skilled public workforce.

- The retirement pledge acknowledges and recognizes the role that public service plays in society.

- Beyond the individual retiree, pension payments generate fiscal and economic advantages.

- Pension plans transfer risk from individual employees to society by guaranteeing income and offering risk pooling.

- Public services that benefit taxpayers are supported by a stable public workforce.

To put it another way, public retirement system funding is a component of the larger social compact that exists between the government, public employees, and society. There are benefits in addition to expenses.

Common arguments and criticisms

The following objections of public retirement schemes that are funded by taxes must also be taken into account:

- Cost to taxpayers: According to some, taxpayers are unjustly paying for public employees’ exorbitant retirement expenses.

- Moral hazard: Taxpayers face hidden risks if public employees demand large pensions regardless of their performance or if governments take on financial risks without sufficient control.

- Intergenerational inequality: Young taxpayers may believe they are footing the bill for past mismanagement or benefits they may not receive.

- Crowding out of services: Government budgets may be increasingly consumed by pension commitments, which would leave less money for other services.

- Benefits that are too generous: Some public pension benefits, according to critics, are higher than those received by employees in the private sector, prompting concerns about fairness.

Looking ahead: Taxpayer funding for public pensions in the future

Public retirement systems’ financial environment is changing. Important trends consist of:

- Rising longevity and shrinking workforces: As people live longer and the ratio of workers to retirees falls, pension costs rise.

- Lower investment returns: Many funds face lower expected returns than historically assumed, raising contribution requirements.

- Demographic shifts: Public-sector workforces may shrink or transform, affecting contributions and benefit formulas.

- Policy innovation: Some states are experimenting with hybrid plans, automatic adjustments, delayed retirement ages, and other reforms.

- Increased transparency and accountability demands: Taxpayers and legislators want clearer data, stress-testing of pension systems, and realistic funding projections.

In conclusion: Why Taxpayers Fund Public Retirement Systems?

Why do taxpayers fund public retirement systems? Because public-service work is essential, retirement benefits help governments recruit and retain talent, pensions stimulate local economies, and society makes a collective promise to those who serve it.

At the same time, the arrangement places significant responsibilities on policymakers, pension administrators, and taxpayers to ensure that funding is adequate, oversight is strong, and intergenerational fairness is maintained.

For a nation committed to public service, the funding of public retirement systems by taxpayers is part of the compact between society and the employees who deliver public goods.

But this compact must be managed wisely. When it is, taxpayers gain long-term value: stable public services, economic activity, and social equity.

How Credit Bureaus Differ: Equifax vs Experian vs TransUnion Explained (2025 Guide)

How Credit Bureaus Differ: Equifax vs Experian vs TransUnion Explained (2025 Guide)