The Role of Private Mortgage Insurance (PMI):

The Role of Private Mortgage Insurance (PMI):

The 20% down payment is a common obstacle to the American dream of home ownership. For many first-time homebuyers, especially in a high-priced housing market, saving that much money can delay or derail homeownership. Private Mortgage Insurance (PMI) can help in this situation.

PMI bridges the gap between affordability and aspiration by enabling buyers to obtain a mortgage with less than 20% down. However, PMI increases expenses in addition to opening doors. Understanding how PMI works, who benefits, and when it may be eliminated is crucial to making wise financial decisions in 2025’s dynamic housing market.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

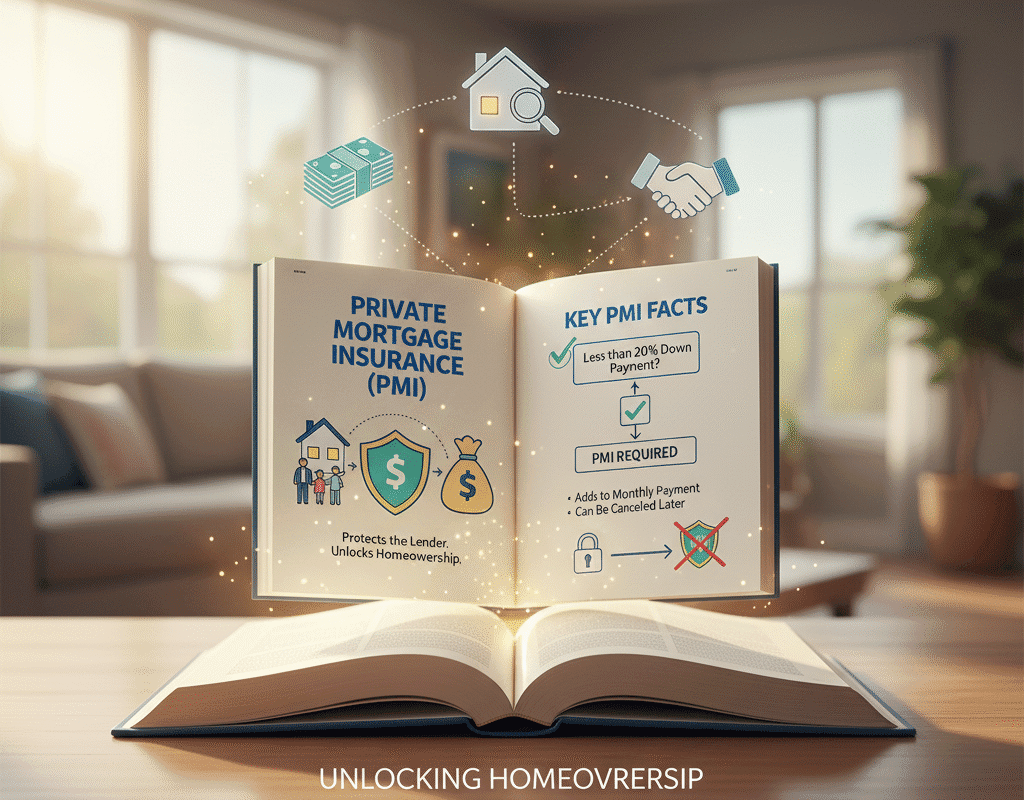

What Is Private Mortgage Insurance (PMI)?

Private Mortgage Insurance is a policy that protects lenders, not borrowers, in case the homeowner defaults on the loan. It’s typically required when a borrower puts down less than 20% of the home’s purchase price on a conventional mortgage.

Here’s how it works:

- The borrower pays monthly premiums for PMI.

- If the borrower stops making payments and the home goes into foreclosure, the insurance company compensates the lender for losses.

While PMI primarily safeguards lenders, it indirectly benefits borrowers by reducing the financial barrier to entry for homeownership.

Why PMI Exists: The Lender’s Perspective

When approving loans, mortgage lenders take on a great deal of risk. A lower down payment means the borrower has less equity and more motivation to walk away if property values decrease. PMI minimizes that risk by ensuring lenders are financially protected against default.

In turn, this protection allows banks and mortgage companies to offer loans to a broader range of buyers, including those who haven’t saved large down payments but have solid credit and stable income.

The Borrower’s Advantage: Accessibility Over Savings

While PMI increases the cost of borrowing, it gives buyers an early pathway into homeownership. Waiting to save 20% could take years—especially as home prices continue to rise nationwide.

For example:

- A $400,000 home with 20% down requires $80,000 upfront.

- With 5% down, the buyer only needs $20,000, though they’ll pay PMI until their equity reaches 20%.

In competitive housing markets like California, Texas, and Florida, PMI often makes the difference between owning and renting.

FHA vs. PMI: What’s the Difference?

PMI applies only to conventional loans. FHA loans, backed by the government, require Mortgage Insurance Premiums (MIP)—similar in purpose but different in structure.

| Feature | PMI (Conventional) | MIP (FHA) |

| Provider | Private insurer | Federal Housing Administration |

| Cancelable | Yes, at 20% equity | Usually after 11 years or never |

| Cost Range | 0.3%–1.5% | 0.8%–1.05% |

| Credit Sensitivity | Based on credit score | Not credit-sensitive |

As conventional loan standards become more flexible in 2025, more borrowers are transitioning from FHA to conventional loans to eliminate long-term insurance costs.

How PMI Impacts the U.S. Housing Market

PMI plays a critical role in stabilizing the housing market and expanding access. Without PMI, millions of Americans would be locked out of homeownership.

According to mortgage industry data:

- Over 30% of homebuyers in 2024 used loans requiring PMI.

- PMI supported nearly $1 trillion in mortgage originations last year.

- The average age of PMI borrowers was 34 years, showing its importance among first-time buyers.

In 2025, as the U.S. faces rising mortgage rates and affordability challenges, PMI continues to function as a financial bridge, allowing more people to buy homes earlier in life.

PMI and First-Time Homebuyers in 2025

For many first-time buyers, PMI is not a burden but a necessary tool for opportunity. With home prices in cities like Austin, Miami, and Seattle soaring, saving 20% can feel impossible.

PMI enables younger Americans—often saddled with student loans—to buy homes sooner and start building wealth through equity.

The National Association of Realtors (NAR) notes that buyers who entered the market with PMI between 2015 and 2019 have, on average, seen equity gains of over $60,000 due to home appreciation.

That’s a clear indicator of PMI’s role as a wealth-building mechanism when managed responsibly.

The 2025 Outlook for PMI

Experts predict that PMI will remain a key component of mortgage financing in 2025 and beyond. As inflation stabilizes and interest rates plateau, lenders will rely on PMI to extend credit safely.

Key 2025 PMI trends include:

- AI-driven underwriting: More accurate risk assessments, potentially lowering premiums.

- Digital cancellation requests: Streamlining equity verification and PMI removal.

- New hybrid products: Insurers exploring flexible PMI structures tailored to gig-economy borrowers.

- Policy discussions: Lawmakers revisiting PMI tax deductions and disclosure transparency.

In conclusion: The Role of Private Mortgage Insurance (PMI)

Private Mortgage Insurance may seem like just another fee on a long list of mortgage costs, but its impact on the U.S. housing market is profound. It empowers millions of Americans to buy homes earlier, contributes to market stability, and provides lenders the confidence to lend responsibly.

For borrowers in 2025, the smartest move is to embrace PMI strategically—use it to gain entry into the housing market, build equity, and then plan for its removal.

In an economy where home prices and mortgage rates remain unpredictable, PMI continues to serve as a cornerstone of accessible homeownership in America.

1 Comment