Why the U.S. Still Uses Routing Numbers?

Why the U.S. Still Uses Routing Numbers?

In an era of real-time payments, blockchain technology, and mobile banking apps, one might assume that America’s banking infrastructure runs on cutting-edge digital identifiers. Yet, every time someone in the U.S. sets up a direct deposit, wires money, or pays a bill online, they still need a nine-digit routing number — a system designed more than a century ago.

So why, in 2025, does the United States still rely on this seemingly outdated system? The answer lies in a combination of regulatory inertia, institutional stability, and the complex structure of the American financial system.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

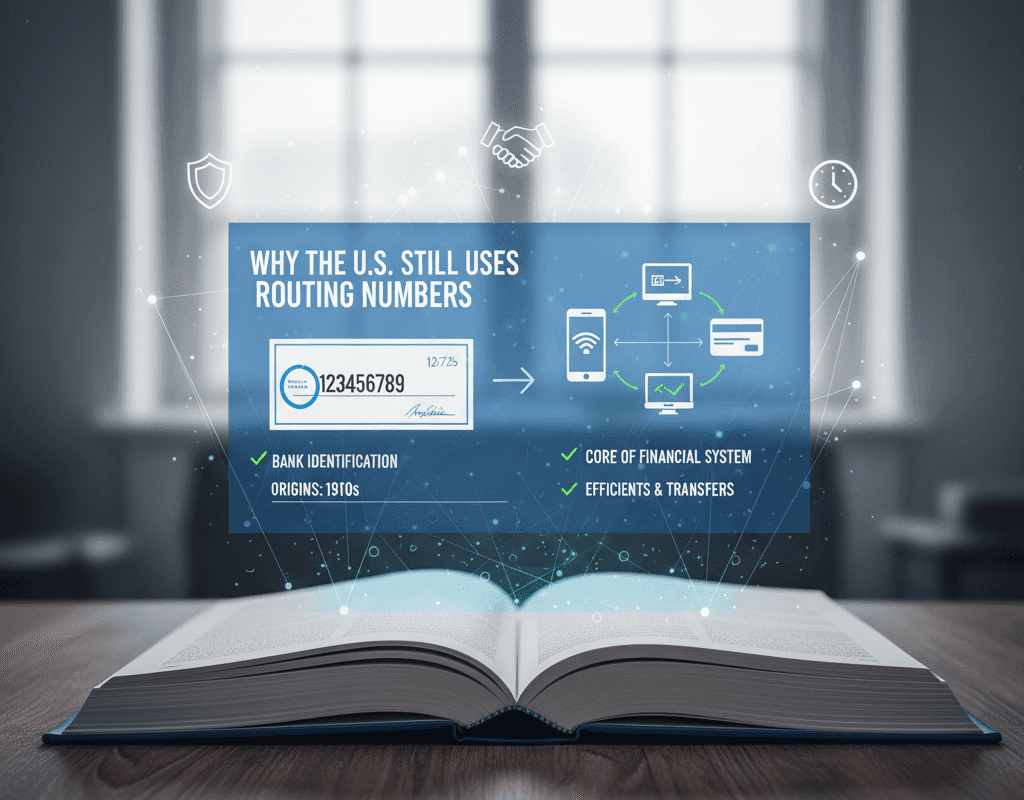

The History: A System Established in 1911

The American Bankers Association (ABA) implemented the routing number system in 1911. The banking system in the United States was dispersed at the time, with thousands of small and regional banks writing checks. Every check had to have a clear method of identifying the bank from which it originated and the address to whom payment should be made.

The ABA Routing Transit Number (RTN), a straightforward numerical code written on each paper check to aid sorting machines in effectively routing payments, was thus created.

Before computers, it connected transactions to particular financial institutions across the nation by acting as a postal address for money.

The Current Operation of Routing Numbers

Every nine-digit route number has a narrative. The numbers indicate:

- Federal Reserve District (first four numbers)

- particular credit union or bank

- Verify the digit (to find errors)

These numbers continued to be the foundation of interbank discussions even when payments shifted online.

Similar to how the postal service uses ZIP codes, your bank’s systems still employ routing numbers to determine where the money should go when you send money via ACH.

One reason routing numbers have persisted is because they are consistent, functional, and accepted by all U.S. banks and credit unions.

The Technological Paradox: Modern Payments on an Old Backbone

To outsiders, it’s puzzling that one of the world’s most advanced economies still leans on a century-old numbering system. After all, countries like the U.K. and European Union have adopted the IBAN (International Bank Account Number) and SWIFT/BIC systems to streamline global transfers.

But the U.S. payment landscape evolved differently.

- The U.S. banking system is highly decentralized, composed of over 4,500 banks and 5,000 credit unions — each with unique operational setups.

- Routing numbers provide a consistent identifier across this diverse landscape, ensuring compatibility between old and new technologies.

The Irony: An Outdated System That Works Remarkably Well

Despite its age, the routing number system continues to perform effectively. Transactions clear daily between millions of banks and consumers without chaos or confusion.

The Federal Reserve’s Fedwire network still depends on these identifiers to transfer over $5 trillion daily.

While other nations have shifted to digital identifiers or blockchain-based systems, the U.S. routing number system’s reliability keeps it relevant.

It’s an irony of modern finance: the “antique” number system is one of the few things keeping America’s financial infrastructure stable.

The Role of Routing Numbers in ACH and Fedwire Transfers

- ACH (Automated Clearing House):

When you send money through services like Zelle, Venmo (bank-linked transfers), or direct deposit, you’re using the ACH network — which depends on routing numbers.

Every ACH entry requires both the sender’s and recipient’s routing numbers to ensure funds move between correct institutions.

- Fedwire:

Used primarily by banks and corporations for large-value transfers, Fedwire also uses routing numbers to identify participants.

Even in high-speed, high-security transfers, the old numeric identifiers remain critical for routing messages within the system.

FedNow and the Future of Instant Payments

In 2023, the Federal Reserve launched FedNow, a real-time payment platform allowing 24/7/365 instant transfers between U.S. financial institutions.

Many expected FedNow to phase out routing numbers, but instead, it integrated them into its architecture.

Why?

Because every participating institution in FedNow must still be identifiable within the broader U.S. banking ecosystem — and routing numbers provide that identity.

This decision reflects a practical reality: innovation in U.S. finance tends to layer over legacy systems rather than replace them.

The Counterargument: “If It’s Not Broken, Don’t Fix It”

Supporters of the current system counter that:

- The U.S. already has efficient domestic payment systems like ACH, RTP, and FedNow.

- Routing numbers are reliable and stable; outages are extremely rare.

- The cost of migration would outweigh potential efficiency gains.

- Many Americans still use checks and traditional banking, especially in small towns and rural areas.

In short, modernization might please technologists but disrupt millions of everyday transactions.

Conclusion: Why the U.S. Still Uses Routing Numbers?

Although it dates back to the early 20th century, the U.S. routing number system is still one of the most dependable and secure foundations of contemporary finance.

From tiny paychecks to billion-dollar wire transfers, it still makes trillions of transactions possible every day.

The longevity of route numbers serves as a reminder that, in a time where innovation is our obsession, sometimes advancement entails improving the status quo.

A living link between the past and the future of American banking, the nine digits at the bottom of a check continue to steer the country’s money even as the country’s financial system moves toward faster, more digital payments.

1 Comment