How Required Minimum Distributions (RMDs) Work?

How Required Minimum Distributions (RMDs) Work?

One of the most important—and misinterpreted—aspects of financial planning for millions of Americans approaching retirement is Required Minimum Distributions (RMDs). RMDs control the amount and timing of withdrawals from tax-deferred retirement accounts, including 403(b)s, 401(k)s, and traditional

Knowing how RMDs operate is important for protecting your nest egg and reducing needless taxes or penalties, not only for adhering to IRS regulations. In order to guarantee that retirees finally pay taxes on monies that have accumulated tax-deferred for years, the Internal Revenue Service (IRS) mandates these distributions.

The RMD landscape is shifting once more in 2025 as new regulations from the SECURE Act 2.0 and inflation adjustments go into effect.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

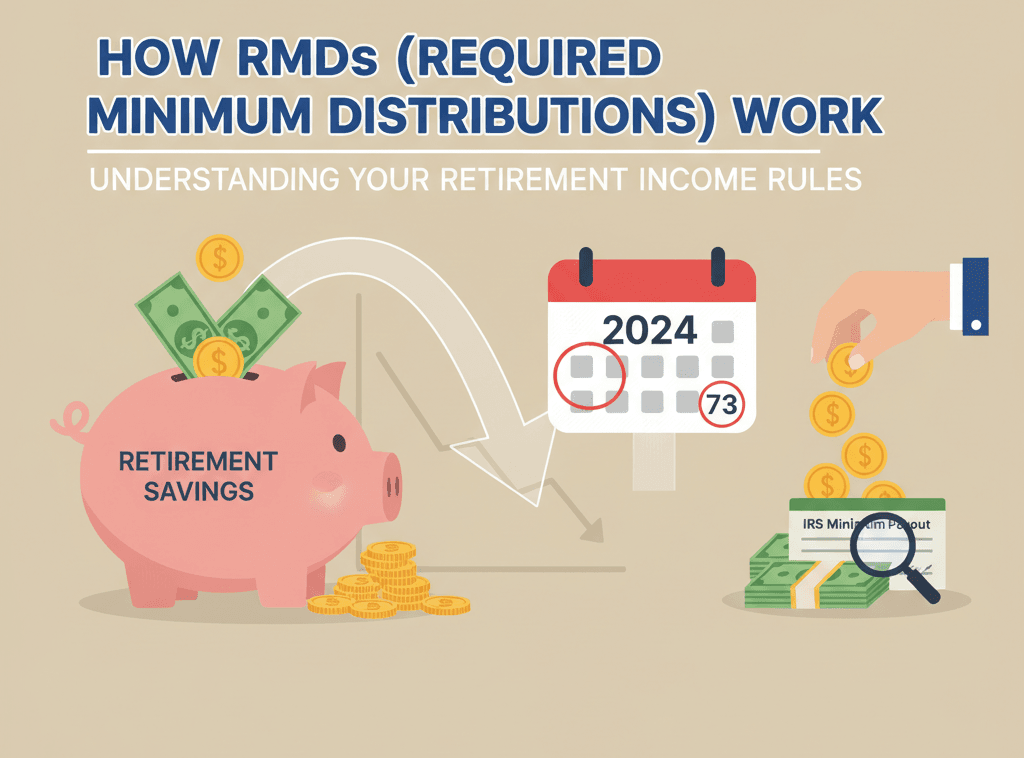

Required Minimum Distributions (RMDs): What Are They?

After reaching a specific age, retirees are required to take annual distributions from their tax-deferred retirement accounts known as Required Minimum Distributions (RMDs). In the year that they are taken out, these distributions are considered taxable income.

The goal is simple: the IRS permits tax-deferred development while you are employed, but it anticipates collecting taxes in the future. RMDs prevent people from holding money in tax-deferred accounts indefinitely.

RMD Age and Rules for 2025

The age at which RMDs begin has shifted multiple times over recent years. The SECURE Act of 2019 raised the age from 70½ to 72. Then, SECURE Act 2.0, signed in late 2022, pushed it even further.

Here’s the current schedule:

| Year of Birth | RMD Start Age |

| 1950 or earlier | 72 |

| 1951–1959 | 73 |

| 1960 or later | 75 |

First-Year RMD Deadline and Timing

The first RMD must be taken by April 1 of the year after you reach your RMD age. Subsequent RMDs must be taken by December 31 each year.

Example:

- If you turn 73 in 2025, your first RMD is due by April 1, 2026.

- Your second RMD (for 2026) is due by December 31, 2026.

Failing to take an RMD on time can trigger a 50% penalty on the amount that should have been withdrawn — though SECURE Act 2.0 reduced this to 25%, and even as low as 10% if corrected promptly.

RMDs from Multiple Accounts

If you have several retirement accounts, RMD rules vary by type:

- Multiple IRAs: You can calculate the total RMD across all and take it from one or several accounts.

- 401(k)s: You must take separate RMDs from each plan.

- 403(b) plans: You can aggregate RMDs and take from one account.

These distinctions are crucial for avoiding accidental under-withdrawals.

Techniques for Reducing RMD Taxes

Your RMD burden can be greatly decreased with careful planning. In 2025, financial advisors suggest the following main strategies:

- Roth Conversions Prior to RMD Age

Convert portions of your traditional IRA into a Roth IRA before RMDs start. You’ll pay taxes now but eliminate future RMD obligations.

- Qualified Charitable Distributions (QCDs)

If you’re charitably inclined, a QCD allows you to donate directly from your IRA, satisfying your RMD and lowering taxable income.

- Delaying Retirement Plan Withdrawals

If you’re still working at 73 and don’t own more than 5% of your employer’s business, you can delay RMDs from your current employer’s 401(k) until retirement.

- Take Into Account Partial Withdrawals Prior to RMD Age

Future RMD sizes can be decreased by beginning smaller withdrawals early (when in a lower tax rate).

- Make Strategic Use of Several Accounts

Withdraw from accounts that make the most tax sense — for example, traditional IRA before taxable brokerage if you want to control income levels.

Common RMD Mistakes to Avoid

- Missing the deadline — leading to unnecessary penalties.

- Forgetting an old 401(k) from a previous employer.

- Incorrectly calculating RMDs on inherited accounts.

- Taking RMDs from the wrong account type.

- Ignoring the tax impact on Medicare premiums.

Keeping a year-end checklist and working with a tax advisor can prevent these common errors.

The Impact of RMDs on Medicare and Social Security

RMDs can increase your adjusted gross income (AGI), which affects:

- Social Security taxation (up to 85% may become taxable)

- Medicare Part B and D premiums (through IRMAA surcharges)

Careful coordination of RMD timing, charitable giving, and Roth conversions can help manage these thresholds.

Couples’ RMD Planning

By diversifying their assets and smoothing their income, married couples can maximize their RMDs:

- If one spouse is younger, the RMD calculation uses the Joint Life Expectancy Table, which can reduce required withdrawals.

- Couples can coordinate Roth conversions strategically across years to minimize total tax exposure.

Joint planning helps reduce the long-term tax burden — especially if one spouse passes away, leaving the survivor in a higher single tax bracket.

Important Lessons

- RMDs are mandatory withdrawals from most retirement accounts starting at age 73 (or 75 for younger cohorts).

- Failure to withdraw can result in stiff penalties — now 25%, reducible to 10% if corrected quickly.

- Roth accounts are generally exempt during your lifetime.

- Tax planning through QCDs and Roth conversions can significantly reduce long-term liability.

- Stay updated on SECURE Act 2.0 changes and IRS guidance each year.

The Last Word: How Required Minimum Distributions (RMDs) Work?

Required Minimum Distributions are one of the most effective tools for retirement planning, despite the fact that they may appear to be simply another IRS formality.

The difference between “taking your RMD” and managing it intelligently can result in years of extra financial security as well as thousands of dollars in tax savings.

To maximize their hard-earned earnings in 2025 and beyond, retirees should concentrate on timely compliance, tax efficiency, and proactive planning.

Why Some U.S. States Have No Income Tax — What It Means For Residents

Why Some U.S. States Have No Income Tax — What It Means For Residents