How the Federal Funds Rate Affects Loans?

How the Federal Funds Rate Affects Loans?

One of the most crucial instruments in US monetary policy is the Federal Funds Rate. The Federal Reserve sets and modifies this benchmark interest rate, which has significant effects on businesses, consumers, and the overall economy. While many headlines focus on whether the Federal Reserve raises or lowers rates, the real question for most Americans is simpler: how does the Federal Funds Rate affect loans?

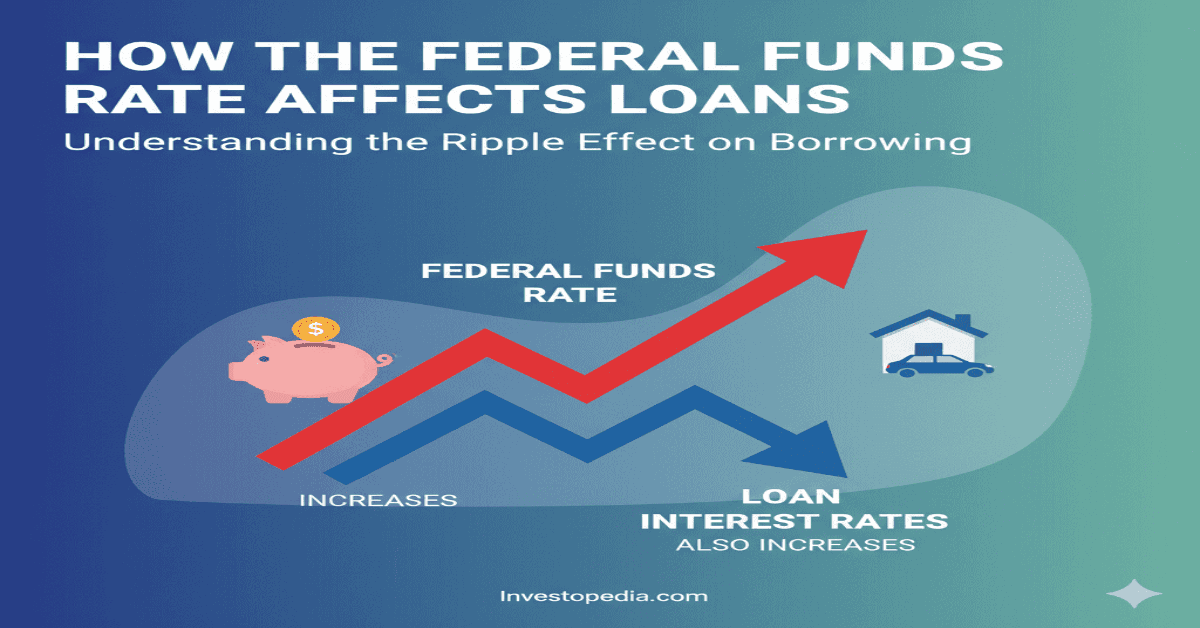

From mortgages to auto financing, credit cards, and small business loans, the Federal Funds Rate indirectly shapes the cost of borrowing. When the rate rises, loans generally become more expensive; when it falls, borrowing tends to get cheaper.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

Federal Funds Rate: What Is It?

The interest rate at which commercial banks lend reserve balances to one another overnight is known as the Federal Funds Rate, or simply the “Fed Funds Rate.” This rate sets the tone for the whole U.S. financial system, despite the fact that it may appear technical.

To determine the target range for the Federal Funds Rate, the Federal Reserve’s FOMC, or Federal Open Market Committee, meets on a regular basis. Economic growth, employment levels, and inflation all have an impact on their choice.

- The Fed often raises the rate to curb spending when inflation is strong.

- The Fed may cut interest rates to promote borrowing and boost demand when the economy slows.

How the Federal Funds Rate Influences Other Interest Rates

Although consumers don’t borrow money directly at the Federal Funds Rate, it acts as a benchmark that ripples across the financial system. Banks and lenders adjust their own rates—on mortgages, credit cards, personal loans, and auto financing—based on movements in the Fed’s rate.

For example:

- A higher Fed Funds Rate usually leads to higher borrowing costs for households and businesses.

- A lower Fed Funds Rate typically results in cheaper loans and financing options.

This indirect influence is why every Fed announcement attracts intense media coverage and why borrowers pay close attention.

Effect on Mortgages

One of the most obvious outcomes of Fed policy is mortgage rates.

Mortgages with fixed rates

- Because fixed mortgage rates are correlated with long-term Treasury yields and market expectations, they frequently fluctuate in response to Fed activities, even though they are not directly connected to the Fed Funds Rate.

- 30-year mortgage rates usually increase when the Fed suggests a higher rate environment, increasing the cost of homeownership.

Mortgages with adjustable rates (ARMs)

- Short-term rates, which fluctuate more immediately with the Fed Funds Rate, are more directly correlated with adjustable mortgages.

- For borrowers with ARMs, a rate increase may result in higher monthly payments, placing a burden on household finances.

Impact of the Housing Market

- Higher mortgage rates reduce affordability, cooling demand in the housing market.

- Lower rates often boost home sales and refinancing activity, stimulating related industries like construction and real estate.

Effect on Auto Loans

Interest rate fluctuations have a significant impact on the automotive sector.

- Auto loan interest rates rise in response to Fed rate hikes, raising monthly car payments. Customers can put off buying a new car or choose less expensive models.

- Lower interest rates make it easier to finance a car, which benefits automakers and dealerships and frequently leads to an increase in car sales.

The Federal Funds Rate has a significant impact on the demand for cars since the majority of Americans finance their car purchases.

Effects on Credit Cards

One of the things that is most immediately impacted by changes in the Federal Funds Rate is credit cards.

- Variable annual percentage rates (APRs) on the majority of credit cards are linked to the prime rate, which is based on the Fed Funds Rate.

- A rate increase raises the cost of carrying debt by making credit card balances instantly more expensive.

- A rate drop reduces annual percentage rates (APRs), which makes managing revolving balances marginally less expensive for customers.

Because of this direct correlation, households that already have credit card debt are immediately impacted by Fed policies.

Effect on Student Loans

The manner that different student loans react to Fed policy varies.

- Congress sets the annual fixed rates for federal student loans, which may not fluctuate in response to changes in the Fed Funds Rate.

- However, variable interest rates associated with private student loans are often linked to market benchmarks that fluctuate in tandem with the Fed.

As a result, payment levels for families and students with private school debt may change based on Fed decisions.

Effect on Business Loans

Loans are essential for funding operations, expansions, and investments for both companies and small businesses.

- Increased Fed Funds Rates make borrowing more expensive, which deters growth and occasionally results in slower hiring or lower expenditure.

- Reduced interest rates facilitate access to finance, which incentivizes companies to undertake expansion investments, acquire equipment, or recruit more employees.

The way the business community responds to changes in interest rates has a big impact on how well the US economy is doing overall.

The Wider Economic Effect

The Federal Funds Rate influences not just individual loans but also the direction of the whole economy.

- Manage of Inflation: The Fed helps manage inflation by lowering consumer demand through rate increases.

- Employment: Lower rates frequently encourage employment and corporate investment, which increases the number of jobs created.

- Stock Market Reaction: Rate hikes frequently cause market volatility, and investors read Fed actions as indicators of future economic prospects.

As a result, the Fed Funds Rate is a major concern for businesses, governments, and international markets in addition to borrowers.

Examples from History

It is clear by looking at history how the Federal Funds Rate affects loans:

The Financial Crisis of 2008

In an effort to promote borrowing and stabilize markets, the Fed cut interest rates to almost zero. Car sales gradually rebounded, and mortgage refinances increased.

Pandemic of COVID-19 (2020)

Mortgage rates reached all-time lows as rates once more fell close to zero. The demand for homes increased dramatically, and business and auto loans became more accessible.

Increase in Inflation in 2022–2023

The Fed aggressively hiked rates in response to the biggest inflation in forty years. APRs on credit cards increased over 20%, mortgage rates soared above 7%, and customers had to pay more for a variety of loan products.

How Customers Can Get Ready for Rate Adjustments

People can make better financial decisions if they understand how the Fed Funds Rate impacts loans:

- Prior to anticipated increases, lock in fixed rates.

- When interest rates are rising, pay off variable-rate debt, such as credit cards.

- Shop around for lenders during periods of lower rates to secure better financing.

- Budget for higher payments if carrying adjustable-rate loans.

Proactive planning can soften the financial impact of shifting interest rate environments.

In conclusion: How the Federal Funds Rate Affects Loans?

Despite appearing to be a technical number that only bankers and legislators should be concerned with, the Federal Funds Rate has an impact on every aspect of American society. This standard influences the cost of financing for both people and businesses, ranging from credit cards and business borrowing to mortgages and vehicle loans.

Businesses can plan investments, consumers can make educated decisions, and policymakers may overcome economic obstacles by knowing how the Fed Funds Rate impacts lending. The Federal Funds Rate will continue to be at the forefront of financial discourse as the United States deals with changing inflation pressures, employment patterns, and international uncertainty.

How Education Levels Shape Economic Growth in the U.S. and Beyond

How Education Levels Shape Economic Growth in the U.S. and Beyond