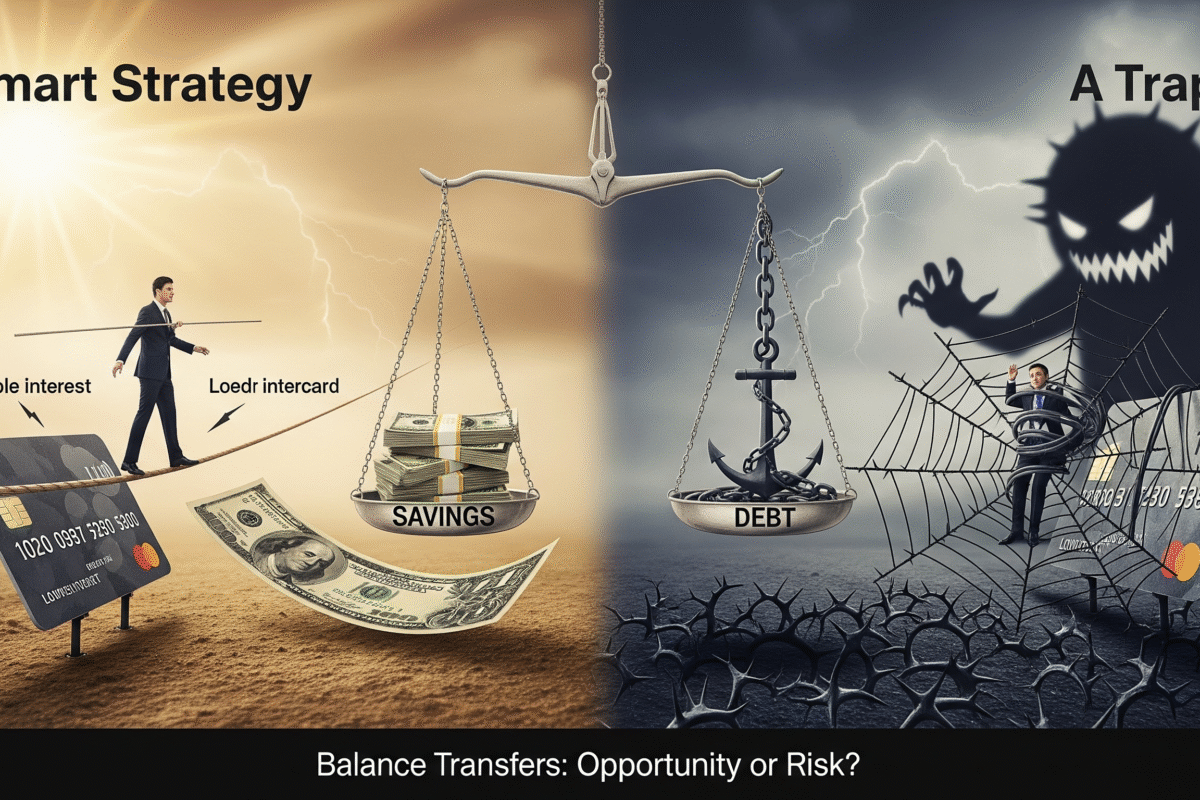

Balance Transfers: Smart Strategy or Dangerous Trap?

Balance Transfers: Smart Strategy or Dangerous Trap?

In today’s high-interest credit card environment, balance transfers have become a hot topic in personal finance. Credit card companies frequently advertise 0% APR balance transfer offers for 12, 15, or even 21 months. On the surface, it sounds like a financial lifesaver—shift your debt, avoid interest, and pay it off faster.

But are balance transfers truly a smart debt strategy, or could they be a trap that worsens financial problems in the long run? In this comprehensive report, we’ll break down how balance transfers work, the advantages, hidden dangers, and real-life strategies to determine whether they are worth considering in 2025.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

What Is a Balance Transfer?

A balance transfer is when you move debt—typically credit card debt—from one account to another, usually to take advantage of a lower interest rate or a promotional 0% APR offer.

For instance:

- You owe $5,000 on a credit card with a 25% interest rate.

- Another bank offers a credit card with 0% APR for 18 months on balance transfers, plus a 3% transfer fee.

- You move your $5,000 balance. Now you only owe a $150 fee and get 18 months to pay down your debt without interest.

Sounds like a win, right? Let’s look closer.

The Informed Aspect of Equilibrium Transfers

Balance transfers have the potential to be an effective debt reduction strategy when implemented properly.

Get Out of Debt with High Interest Rates

Repayment of debt is very costly in the United States, where the average annual percentage rate (APR) for credit cards is now over 21%. There is leeway to pay down principal rather than interest with a 0% APR transfer.

Reduce Debt More Quickly

Every dollar goes straight toward lowering your balance—there is no interest involved. You may pay off your debt considerably more quickly if you maintain your discipline.

Make Finances Easier

It may be simpler to monitor and control repayment if several sums are transferred to a single card.

Potentially raise your credit score

If managed responsibly, lowering your utilization rate and making on-time payments could improve your credit profile.

The Drawbacks of Equilibrium Transfers

Regretfully, a lot of people make common mistakes.

The Total of Transfer Fees

Typically, 3% to 5% of the transferred amount is charged for balance transfers. On $10,000, that’s $300–$500 immediately added to your debt.

Temporary Relief Only

When the promotional period ends, interest rates often skyrocket—sometimes higher than your original card.

Temptation to Spend More

One of the biggest risks is freeing up credit on your old card and then using it again, leading to double debt.

Credit Score Risks

Applying for a new credit card requires a hard inquiry, which may temporarily lower your credit score. If you max out the new card, your utilization may also harm your score.

Math for Balance Transfer: Actual Example

Let’s use numbers to analyze it.

- Balance on original card: $6,000 at 24% APR

- New Card Offer: 3% transfer fee, 18 months at 0% APR

- Fee: $180

- Monthly Payment (to pay off in promo period): $6,180 ÷ 18 = $343/month

`Following this method will save you hundreds of dollars in interest while only costing you $180 in fees.

However, if you merely pay the minimum, interest rises to 25% and the promotion expires. Now your balance remains high, and you may be worse off.

For whom are balance transfers appropriate?

Balance transfers are most effective for:

- Good to exceptional credit is required for approval.

- borrowers with reasonable repayment plans during the promotional time and manageable debt (often under $15,000.

- disciplined consumers who refuse to use the previous card.

Who Must Steer Clear of Balance Transfers?

They pose a risk because

- those who are unable to pay on a regular basis.

- Low credit score borrowers are less likely to be eligible for favorable offers.

- Someone who is prone to accrue additional debt on other credit cards.

- those with balances that are too high to settle during the promotional period.

The Psychology of Balance Transfers

Debt is not only financial—it’s emotional. The sense of relief from moving debt can create a false sense of progress. Behavioral experts warn that without habit changes, many people repeat the cycle of overspending, balance transfers, and continued debt.

Tips for Using Balance Transfers Wisely

- Calculate the Real Cost – Factor in fees and deadlines.

- Set a Payment Plan – Divide total debt by promo months and stick to it.

- Avoid New Purchases – Only use the card for the transfer.

- Pay More Than the Minimum – Always.

- Mark the End Date – Set reminders before the 0% APR expires.

- Check the Fine Print – Some offers exclude cash advances or have special rules.

In Conclusion

In the end, a balance transfer is a financial tool—neither good nor bad on its own. Like a sharp knife, it can either cut your debt or cut deeper into your financial health.

If you approach it with discipline, awareness of fees, and a clear plan, balance transfers can save thousands of dollars and speed up debt freedom. But if used recklessly, they can lead to even greater debt burdens.

The smartest move? Know yourself, know your habits, and use balance transfers cautiously.