Renters Insurance: Do You Really Need It?

Renters Insurance: Do You Really Need It?

For millions of Americans, renting is frequently the more sensible option in the current housing market. In the United States, more than 44 million households rent, according to the U.S. Census Bureau. However, even though renting is so popular, a startlingly high percentage of tenants neglect a crucial safety measure: renters insurance.

This begs the important question: Is renters insurance truly necessary? Or is it simply one more monthly cost you can do without?

We’ll go over everything you need to know about renters insurance in this in-depth guide, including what it covers, what it doesn’t, how much it costs, and if it makes sense for you in 2025.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

Renters insurance: what is it?

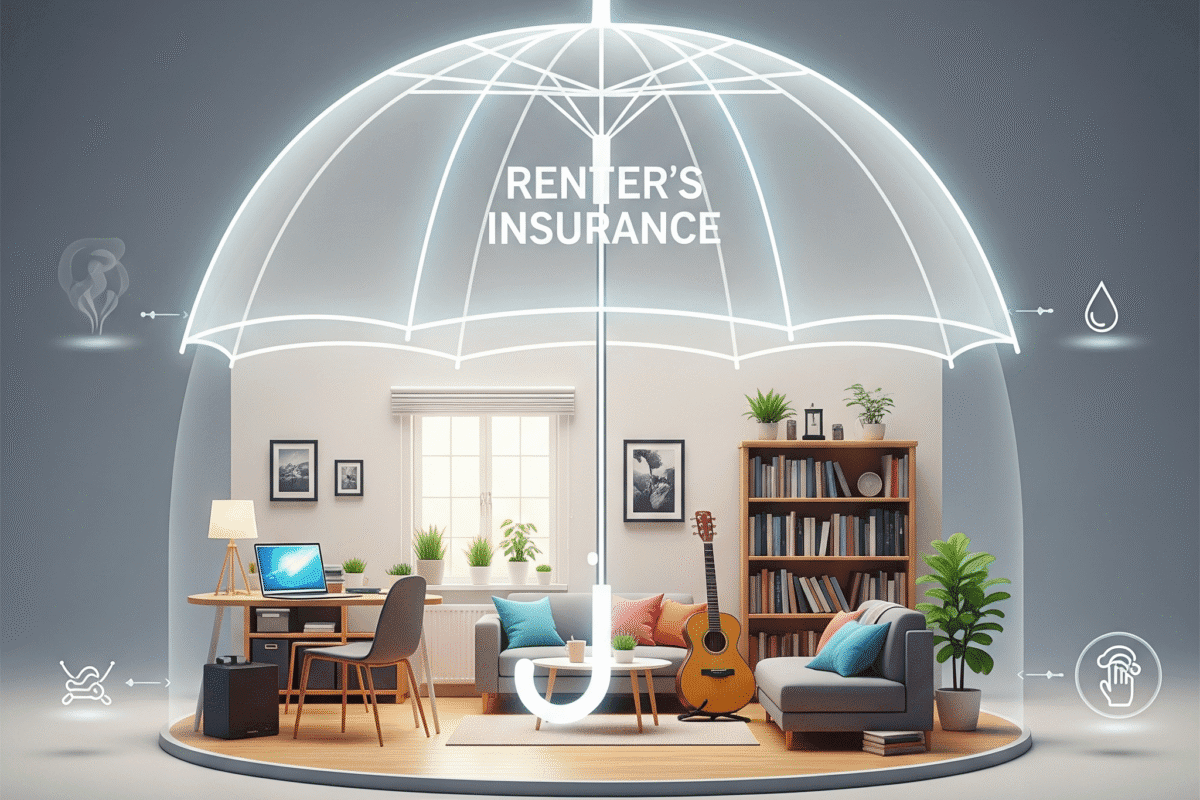

A sort of policy called renters insurance is intended to safeguard those who rent their properties, whether they are houses, apartments, or condos. It does not cover the building itself, which is the responsibility of your landlord, in contrast to homeowners insurance. Rather, it concentrates on your personal property, liability coverage, and extra living costs in the event of an emergency.

It is, in essence, financial security for your life in a rental home.

What Is Covered by Renters Insurance?

Three primary areas are usually covered by renters insurance:

Individual Property

The main justification for purchasing renters insurance is this. Your insurer assists in replacing your possessions in the event that they are stolen or damaged as a result of covered risks, sometimes known as “perils.”

Typical covered risks consist of:

- Damage from smoke and fire

- Burglary and theft

- Vandalism

- Water damage (not from floods) caused by plumbing problems

- Some natural calamities, such as hailstorms and windstorms

Imagine your clothes, TV, laptop, or furniture being destroyed in a fire. You would have to pay cash if you didn’t have insurance. You might receive reimbursement through renters insurance.

Defense Against Liability

You can be held legally liable if someone is hurt in your rental property, such as if a visitor trips and falls on a wet floor. Liability coverage helps pay for medical bills, legal fees, and damages.

For instance:

- Your dog bites a visitor.

- You accidentally cause a kitchen fire that damages your neighbor’s unit.

- Without liability coverage, you might face thousands of dollars in expenses.

Additional Living Expenses (ALE)

If your rental becomes uninhabitable due to a covered event (like a fire), ALE pays for temporary housing, meals, and other extra costs while repairs are made.

Things Not Covered by Renters Insurance

It’s equally critical to understand what is not covered by renters insurance:

- Earthquakes and floods need different policies.

- Termite, rodent, and bed bug infestations are not covered.

- Property of Roommates ↑ Every renter requires a different policy.

- Luxury Items Over Limits: Collectibles, jewelry, and artwork could require extra riders.

What is the cost of renters insurance in the United States in 2025?

The affordability of renters insurance is among its most alluring features.

According to the National Association of Insurance Commissioners (NAIC), the average cost of renters insurance in the U.S. is about $15–$25 per month (or $180–$300 per year).

Price-influencing factors include:

- Your location (high-crime or disaster-prone areas may cost more)

- Amount of coverage you choose

- Deductible (the amount you pay before insurance kicks in)

- Whether you bundle with auto insurance

For the cost of a few cups of coffee each month, renters insurance provides thousands of dollars in protection.

Does Renters Insurance Make Sense? Benefits and Drawbacks

Let’s consider the advantages and disadvantages.

Advantages:

- Reasonably priced ⇒ Under $1 per day.

- safeguards possessions, including clothing, furniture, electronics, and more.

- Liability protection → prevents expensive lawsuits.

- covers additional living costs in case of an emergency.

- Many landlords need → Avoids lease violations.

Cons:

- Doesn’t cover everything (floods, earthquakes, luxury items).

- Monthly expense even if you never make a claim.

- Deductible means small losses may not be worth filing.

How to Pick the Best Policy for Renters Insurance

When shopping for renters insurance, consider these steps:

- Take Inventory of Your Belongings → List items and estimate value.

- Decide Coverage Limits → Ensure your policy covers replacement cost, not just actual cash value.

- Compare Quotes → Use online comparison tools to get the best deal.

- Check Policy Exclusions → Know what’s not covered.

- Bundle with Auto Insurance → Many companies offer discounts.

USA’s Top Renters Insurance Providers (2025)

These are some of the best choices based on coverage, customer service, and affordability:

- State Farm – Great nationwide availability.

- Allstate – Strong discounts and online tools.

- Lemonade – Tech-driven and fast claims process.

- USAA – Best for military families.

- Progressive – Easy bundling with auto insurance.

Important Takeaways

- Renters insurance is affordable and offers peace of mind.

- It covers personal property, liability, and additional living expenses.

- It’s not legally required everywhere, but landlords increasingly demand it.

- For less than the cost of a pizza per month, it can save you from financial disaster.

So, do you really need renters insurance?

Understanding Risk Tolerance in Investing: A Complete Guide for Smart Investors

Understanding Risk Tolerance in Investing: A Complete Guide for Smart Investors