Tax-Advantaged Investment Accounts in the U.S. (2025 Guide):

Tax-Advantaged Investment Accounts in the U.S. (2025 Guide): The Importance of Tax-Advantaged Accounts Has Increased

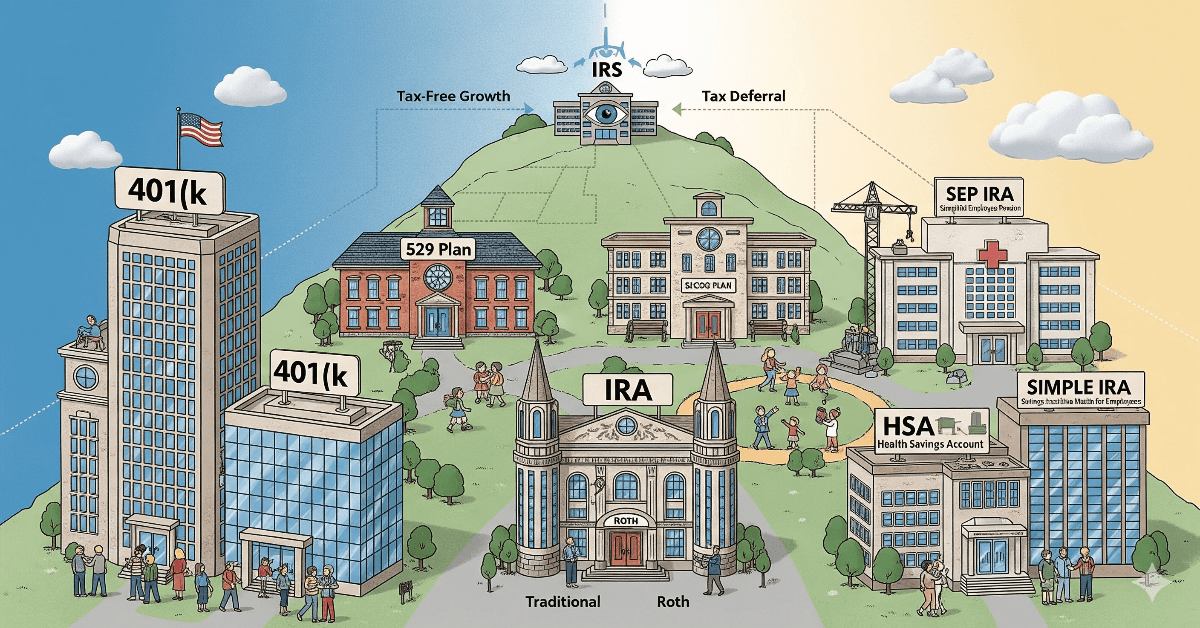

Concerns about retirement preparation, market volatility, and growing living expenses are still issues facing American investors in 2025. Using tax-advantaged investment accounts is one of the best ways to increase wealth and lower taxable income. Depending on the kind, these accounts, which include IRAs, 401(k)s, HSAs, and 529 plans, provide benefits including tax deductions, tax-free growth, or tax-free withdrawals.

Understanding these accounts is essential as federal tax regulations change and retirement becomes a major concern for millions of Americans. The primary categories of tax-advantaged accounts, their regulations in 2025, contribution caps, and methods for optimizing benefits are all covered in detail in this article.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

IRAs, or individual retirement accounts

Conventional IRA

Among the most widely used retirement accounts is still the Traditional IRA. Contributions are often tax-deductible, and investments grow tax-deferred until withdrawals in retirement.

- 2025 Contribution Limit: $7,000 (with an extra $1,000 catch-up for those over 50).

- Tax Benefit: Upfront deduction, lowering taxable income.

- Withdrawals: Taxed as ordinary income; penalties apply before age 59½ unless exceptions apply.

The Roth IRA

The reverse of this is a Roth IRA. While retirement payouts are tax-free, contributions are after-tax. Younger investors who anticipate greater tax rates in the future may find it more alluring because of this.

Contribution cap for 2025: $7,000 ($1,000 catch-up for those over 50).

- Income Phase-Outs: “Backdoor Roth IRA” options are still accessible, however high earners may be subject to restrictions.

- Tax Benefit: Both growth and withdrawals are exempt from taxes.

The main distinction between traditional and Roth IRAs

- Tax break now, taxes later with a traditional IRA.

- Taxes now, tax-free later with a Roth IRA.

Retirement Plans Sponsored by the Employer 401(k) Plans

The foundation of American retirement savings is still the 401(k).

2025 $23,000 is the maximum contribution ($7,500 for those over 50).

Employer Match: A lot of firms make extra financial contributions.

Taxation: Roth 401(k) contributions are made after taxes, while traditional 401(k) contributions are made before taxes.

Plans 403(b) and 457

For public sector workers, 403(b) (teachers, nonprofits) and 457(b) (state and local government employees) function similarly to 401(k)s with comparable contribution limits.

Solo 401(k)

For self-employed professionals, the Solo 401(k) allows higher contributions by combining employee and employer roles.

HSAs, or health savings accounts

Despite being frequently disregarded, the HSA is regarded as the “triple-tax advantage” account:

- Tax deductions are available for contributions.

- Growth is exempt from taxes.

- Tax-free withdrawals are permitted for approved medical costs.

- Contribution caps for 2025 are $4,300 for individuals and $8,600 for families, plus an additional $1,000 for those over 55.

- The money can be utilized for medical expenses in retirement and rolls over from year to year.

HSAs serve as both a retirement savings tool and a healthcare tool.

Education Savings Plans

529 Plans

The 529 college savings plan offers families a way to prepare for rising education costs.

- Contributions: No federal deduction, but many states offer tax incentives.

- Tax Treatment: Growth is tax-free if used for qualified education expenses.

- New Flexibility: As of 2024, unused funds can be rolled into a Roth IRA for the beneficiary (with limits).

Coverdell ESA

Though less popular, Coverdell Education Savings Accounts also provide tax-free growth for educational use but have lower contribution limits.

Other Tax-Advantaged Accounts

SEP IRA

Ideal for self-employed individuals and small business owners. Contributions are tax-deductible, with higher limits compared to a Traditional IRA.

SIMPLE IRA

Designed for small businesses with fewer than 100 employees. Simpler than 401(k) plans but with lower contribution caps.

Annuities

Though not technically a “tax-advantaged account,” annuities provide tax-deferred growth and can complement retirement portfolios.

Tax Law Updates in 2025

Recent changes to tax law have impacted contribution limits and eligibility. In 2025:

- Inflation adjustments raised limits for IRAs, 401(k)s, and HSAs.

- Roth IRA income phase-out thresholds increased slightly.

- 529-to-Roth rollovers became more widely adopted after 2024’s SECURE 2.0 Act provisions.

These updates make tax planning in 2025 more complex but also more rewarding.

Techniques to Optimize Advantages

- Utilize Several Accounts: To vary tax treatment, combine an HSA, Roth IRA, and 401(k).

- Maximize Employer Matches: Make sure you always utilize the free employer contributions.

- Plan for Future Tax Brackets: Traditional accounts are more advantageous for high earners, while Roth accounts may be preferred by younger savers.

- Use HSAs for More Than Just Medical Care: Think of your HSA as a covert retirement fund.

- Automate Contributions: Dollar-cost averaging is used in consistent investing.

Typical Errors to Steer Clear of

- Failing to contribute enough to get the full employer match.

- Forgetting about Required Minimum Distributions (RMDs) starting at age 73.

- Using Roth IRA contributions without understanding income limits.

- Treating HSAs as short-term savings instead of long-term growth vehicles.

Tax-Advantaged Accounts’ Future

By 2030, financial experts anticipate possible changes:

- As retirement difficulties intensify, there may be increased contribution caps.

- increased Roth alternatives as a result of the federal government’s need to collect taxes up front.

- increased retirement account and 529 plan connectivity.

Tax-advantaged accounts will probably continue to be a key component of American financial planning while lawmakers struggle with retirement security.

In conclusion, generating wealth in an intelligent manner

Tax-advantaged investment accounts are vital resources for regular Americans to safeguard their future, not just the wealthy. These accounts, which range from 401(k)s and IRAs to HSAs and 529 plans, offer significant tax advantages as well as prospects for long-term development.

Strategic diversification—using many accounts to meet immediate needs and long-term retirement objectives—will be crucial in 2025. Investors may maximize the potential of these accounts and create long-term financial security by being aware of the regulations, contribution caps, and tax benefits.