Dollar-Cost Averaging Explained Simply:

Dollar-Cost Averaging Explained Simply: Investing Doesn’t Have to Be Complicated

When people think about investing, they often imagine watching stock charts all day, stressing over market crashes, or trying to “time” the perfect moment to buy. But what if there was a strategy that took away the guesswork?

That’s where Dollar-Cost Averaging (DCA) comes in. It’s one of the simplest and most powerful investment methods available. Whether you’re saving for retirement, building wealth slowly, or just getting started in the stock market, DCA could be the key to your long-term financial success.

In this article, we’ll break down Dollar-Cost Averaging in simple terms, show you how it works, explore its advantages and disadvantages, and explain how you can start using it today.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

What Is Dollar-Cost Averaging (DCA)?

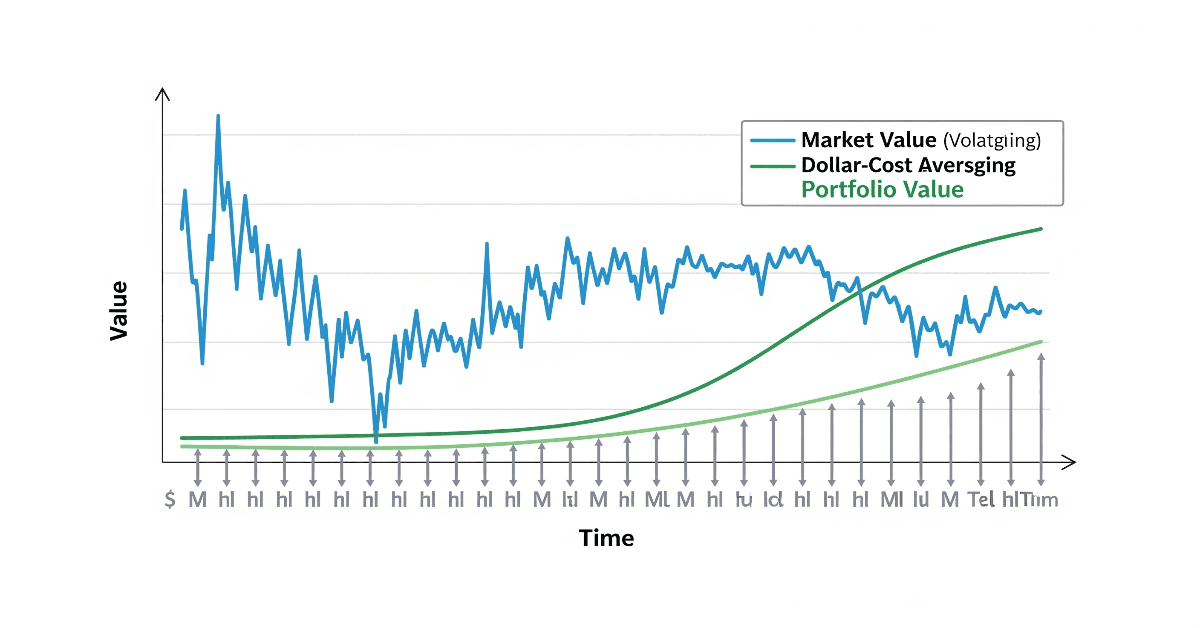

Cost in dollars Averaging is an investment strategy where you invest a fixed amount of money at regular intervals, regardless of whether the market is up or down.

Instead of trying to predict market highs and lows, you invest consistently—say, $200 every month—into the same investment (like an index fund, stock, or ETF).

Over time, this approach means you buy more shares when prices are low and fewer shares when prices are high.

Example of DCA in Action

Imagine you invest $200 per month into a stock:

- January: Stock price = $20 → You buy 10 shares.

- February: Stock price = $25 → You buy 8 shares.

- March: Stock price = $16 → You buy 12.5 shares.

- April: Stock price = $22 → You buy 9 shares.

After four months, you’ve invested $800. Your average cost per share is lower than the average market price because you bought more when the stock was cheap.

That’s the power of Dollar-Cost Averaging.

The Function of Dollar-Cost Averaging

Most investors struggle with emotions—fear during downturns and greed during market highs. DCA removes emotions by making investing automatic and consistent.

Key Benefits:

- Reduces Risk of Market Timing – You don’t need to predict when the market will rise or fall.

- Builds Discipline – Automatic, scheduled investing makes wealth-building a habit.

- Smooths Out Volatility – Instead of worrying about ups and downs, you steadily accumulate assets.

- Accessible to Everyone – You don’t need thousands of dollars to start. Even $50 per paycheck can work.

Historical Proof: Does Dollar-Cost Averaging Work?

- Let’s examine the past. The U.S. stock market has seen crashes, booms, recessions, and recoveries. Yet, long-term investors who kept investing regularly almost always came out ahead.

- During the 2008 Financial Crisis, those who continued investing through DCA bought more shares when prices were low, leading to strong gains once the market recovered.

- Investors who started DCA in the 1990s tech boom and held through the dot-com crash still saw strong returns over 20+ years.

- Even with inflation and recessions, the S&P 500 has averaged about 10% annual returns historically.

- By sticking to DCA, you benefit from time in the market, not trying to time the market.

Comparing Lump-Sum Investing with Dollar-Cost Averaging

- One frequently asked question is: Should I use DCA to spread out my money or invest it all at once (lump sum)?

- Lump-Sum Investing: If you invest $12,000 at once, you immediately benefit if the market rises. Historically, lump-sum investing has slightly outperformed DCA because markets tend to go up over time.

- DCA: Spreading $12,000 over 12 months reduces the risk of investing right before a crash. It’s safer for risk-averse investors or those just starting out.

- The bottom line: If you have a large amount and can handle volatility, lump-sum might work better. But if you value safety and peace of mind, DCA is the smarter choice.

How to Start Dollar-Cost Averaging

Starting with DCA is straightforward. Here’s a step-by-step guide:

Step 1: Decide How Much to Invest

Choose a fixed amount that fits your budget. Even $50 per paycheck is enough to start.

Step 2: Pick Your Investments

Most beginners use:

- Index Funds (e.g., S&P 500 ETF) – Diversified, low-cost, long-term growth.

- Blue-Chip Stocks – Stable, established companies.

- Target-Date Funds – Adjust risk automatically as you approach retirement.

Step 3: Automate Your Contributions

Set up automatic transfers through your brokerage or retirement account. This ensures consistency.

Step 4: Stick With It Through Highs and Lows

The hardest part of DCA is staying consistent. Don’t pause contributions during market dips—those are the best buying opportunities.

The Psychology Behind Dollar-Cost Averaging

One of the biggest reasons DCA works is psychological. Humans naturally want to “buy low and sell high,” but in practice, emotions cause the opposite—panic selling in downturns and buying during bubbles.

Dollar-Cost Averaging removes decision-making. You invest whether the market is up, down, or sideways. Over decades, this consistent discipline creates significant wealth.

Advantages of Dollar-Cost Averaging

- Easy for Beginners – No need to study charts daily.

- Affordable – Works with small amounts of money.

- Automatic Wealth Building – Pairs well with 401(k) or IRA contributions.

- Reduces Stress – No need to worry about “perfect timing.”

- Strong Long-Term Growth – Especially effective in volatile markets.

Disadvantages of Dollar-Cost Averaging

- May Miss Out on Bigger Gains – Lump-sum investing often beats DCA in rising markets.

- Requires Discipline – Skipping contributions reduces effectiveness.

- Slow Growth at First – Returns are gradual, not instant.

- Not Foolproof – If you choose bad investments, DCA won’t save you.

Dollar-Cost Averaging in Different Markets

In Stocks

Perfect for beginners who want to invest in companies without timing the market.

In Cryptocurrency

Since crypto markets are volatile, DCA helps reduce risk by spreading purchases over time.

In Retirement Accounts

401(k) and IRA contributions are essentially DCA in action—automatic investments every paycheck.

Dollar-Cost Averaging’s Drawbacks

Might Lose Out on Greater Profits In rising markets, lump-sum investing frequently outperforms DCA.

Demands Self-Control: Ignoring contributions diminishes efficacy.

First, growth is slow; returns are not immediate.

Not Infallible: DCA won’t help you if you make poor investing decisions.

Dollar-Cost Averaging for Stocks in Various Markets

Ideal for novices who wish to make business investments without having to time the market.

Regarding Cryptocurrency

By distributing purchases across time, DCA helps lower risk in the erratic cryptocurrency markets.

Contributions to 401(k) and IRA retirement accounts are simply DCA in action—automatic investments made with each paycheck.

Common Errors to Steer Clear of

- Stopping During Market Crashes – This ruins the benefit of buying low.

- Investing in High-Fee Funds – Choose low-cost index funds or ETFs.

- Not Having an Emergency Fund First – Always build savings before investing.

- Expecting Quick Riches – DCA builds wealth gradually, not overnight.

Final Thoughts: Why Dollar-Cost Averaging Matters Today

In today’s unpredictable economy, where inflation, interest rates, and global uncertainty shake markets, Dollar-Cost Averaging offers a stress-free way to build wealth.

It’s not about timing the market—it’s about time in the market. Whether you’re investing in stocks, ETFs, crypto, or retirement funds, DCA helps you stay consistent and take advantage of long-term growth.

For beginners, DCA is often the best first step into investing—simple, safe, and effective.