Simple Personal Finance Guide: Budgeting Rule Explained

Simple Personal Finance Guide: Budgeting Rule Explained

Despite being one of the most crucial life skills, money management is frequently not taught in schools. Paying off debt, saving for the future, and controlling spending are challenges that many people face. The 50/30/20 rule is a straightforward budgeting technique that can help you take charge of your money without feeling overburdened.

We’ll explain what the 50/30/20 rule is, how it operates, and why it’s one of the simplest and best budgeting strategies you can employ to reach financial stability in this article.

What is the rule of 50/30/20?

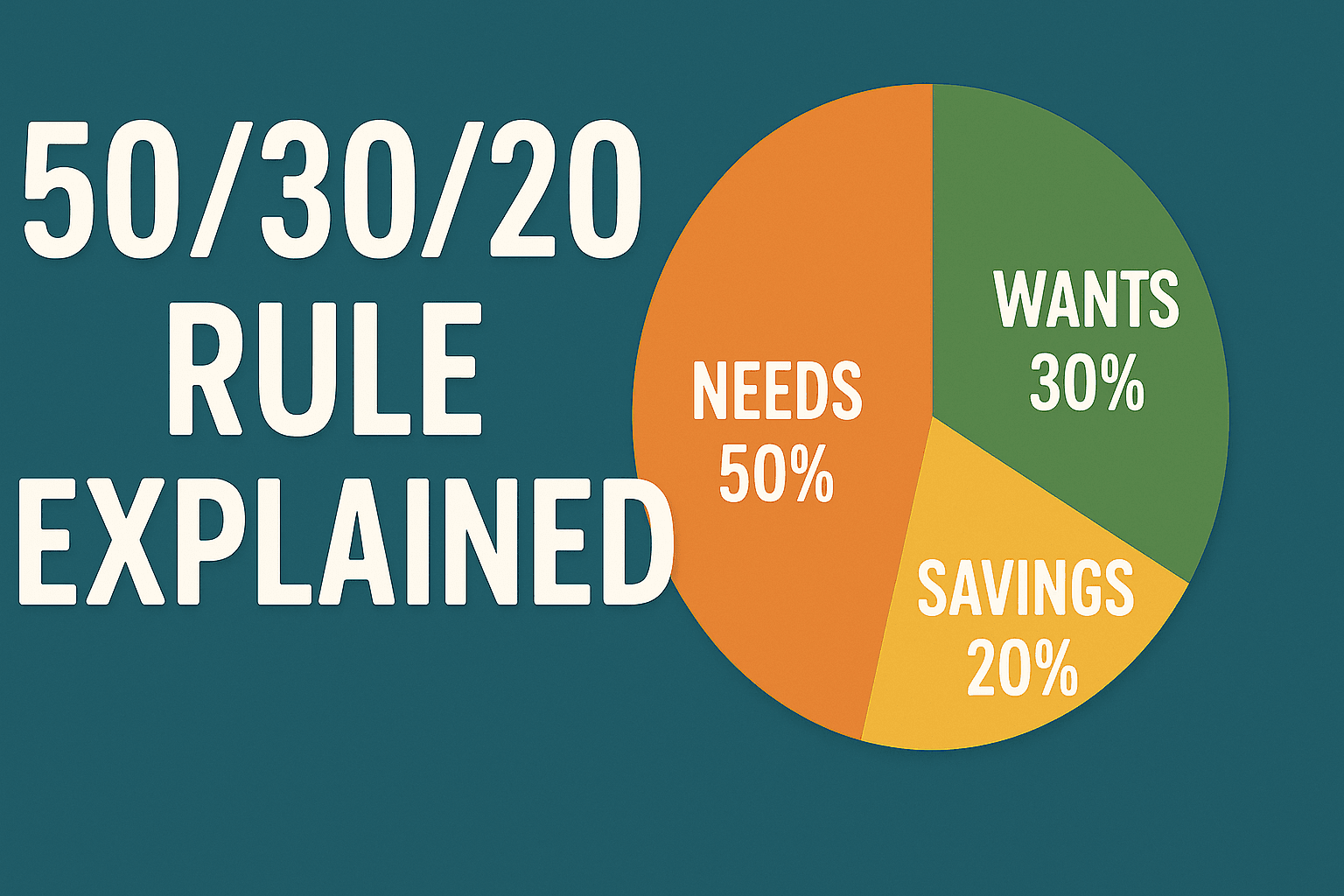

A simple budgeting method known as the 50/30/20 rule splits your post-tax income into three categories:

- 50% goes toward necessities, which include things like shelter, food, utilities, medical care, and transportation.

- 30% goes into wants, which include non-essential expenses like entertainment, eating out, shopping, and trips.

- 20% for Debt Repayment and Savings: This includes investing, paying off credit card or loan debt, and creating an emergency fund.

In her book All Your Worth: The Ultimate Lifetime Money Plan, Senator Elizabeth Warren popularized this idea. The goal is to maintain a straightforward budget while making sure you save for the future, enjoy life, and pay for essential bills.

HSBC Cashback Credit Card 2025 – Benefits, Rewards & How to Apply?

Why the 50/30/20 Rule Is Effective?

The 50/30/20 rule is simple to remember and implement, in contrast to intricate spreadsheets or programs that keep track of every dime. This explains why it works so well:

- Simplicity: There are just three groups of expenses to classify.

- Balance: You’re spending money on leisure and lifestyle in addition to savings.

- Flexibility: The guideline applies to a range of financial objectives and income levels.

- Long-Term Benefits: You can increase your financial security by continuously saving 20%.

Dissecting the 50/30/20 Budget:

- Setting aside 50% for necessities

The costs necessary to live and work are known as needs. These consist of:

- Mortgage or rent

- Gas, electricity, water, and internet utilities; groceries

- Transportation (gas, public transportation, auto payments)

- Medical expenses and health insurance

- The lowest possible loan payments

- Advice: You could need to reduce your expenses by refinancing debt, lowering utility bills, or downsizing your home if your needs exceed 50% of your income.

- Thirty percent for wants

Wants are items that enhance your way of life but are not necessary. Among the examples are: • Dining out • Subscriptions to streaming services (Netflix, Spotify, etc.)

- Purchasing and upscale goods

- Travel and vacations • Hobbies or gym memberships

Advice: The most adaptable category is wants. You can temporarily lower this to 20% or 10% if you’re saving for a significant objective.

- 20% for debt repayment and savings

This part is what positions you for future prosperity and financial stability. It consists of: • Contributions to emergency funds

- Retirement funds (IRA, 401(k))

- Stocks, ETFs, and real estate investments; additional debt repayments for college loans and credit cards;

Advice: Prioritize paying off high-interest debt before making investments. Increase your focus on investing and savings after your debt is under control.

An Illustration of the 50/30/20 Rule in Operation

Assume you earn $4,000 each month after taxes. This is how you would split it:

- $2,000 for 50% of needs (rent, groceries, bills, and insurance)

- Thirty percent want $1,200 for entertainment, dining, and shopping.

- 20% Debt/Savings: $800 (loan repayment, investments, and emergency fund)

Advice: This guarantees that your basic needs are met, that you have fun, and that you are accumulating wealth for the future.

How to Create a Monthly Budget That Actually Works in 2025?

Positive aspects of the 50/30/20 Rule

- Simple to follow: No intricate tracking is required.

- Promotes saving by guaranteeing that 20% is always allocated to long-term objectives.

- Adaptable: Fits most income brackets.

- Prevents overspending by assisting you in recognizing when savings are being depleted by wants.

Objections to the 50/30/20 Rule

Although helpful, this approach isn’t flawless. Among the restrictions are:

- Not universally applicable: Housing alone can account for more than 50% in expensive cities.

- Overly broad: Ignores specific financial objectives, such as early retirement.

- Difficult with inconsistent income: Freelancers may encounter difficulties.

Advice: As an alternative, change the percentages to 60/20/20 or 70/20/10 based on your goals and way of life.

How to Get Started Applying the Rule of 50/30/20

- Utilize your tax returns or pay stubs to determine your after-tax income.

- Make a list of your spending and divide them into savings, wants, and needs.

- Check to see if you’re within 50/30/20 by comparing with the rule.

- Modify: Cut back on necessities, cut back on wants, or boost savings.

- Automate savings: Establish recurring deposits into retirement and savings accounts.

Digital Resources to Assist in Enforcing the Rule

Budgeting can be made simpler with the help of apps and internet resources:

- Mint: Automatically tracks and classifies spending.

- You Need A Budget, or YNAB, assists in allocating each and every dollar.

- Personal Capital: Excellent for monitoring investments and savings.

- Basic spreadsheets: Excel and Google Sheets are both compatible.

Who Needs to Apply the 50/30/20 Rule?

This approach to budgeting works well for: • Young professionals who are just beginning their financial careers.

- Families seeking a straightforward financial strategy.

- People who are overburdened by intricate budgeting.

- Anyone seeking a balance between saving for the future and living in the now.

Adapting the 50/30/20 Rule to Various Circumstances

- Low Income: 60–70% may go toward necessities. Cut saves to 20% and desires to 10%.

- High Income: You can quickly achieve financial independence and save over 20%.

- Heavy Debt: Reduce wants and raise debt payback to 30%.

- Retirement Planning: If at all possible, increase savings to 30–40%.

Common Errors to Steer Clear of

- Mislabeling needs as wants (luxury automobile, premium cable, etc.).

- Ignoring debt: Progress is slowed when minimum payments are made.

- Infrequent review: Monthly budget updates are necessary.

- Spending everything in the desires category: Think about transferring extra funds to savings.

Reasons for the Popularity of the 50/30/20 Rule in 2025

People are looking for straightforward financial methods in the current economy due to rising inflation and increased living expenses. The 50/30/20 rule is becoming more and more popular because:

- It’s simple to follow even if you don’t know much about finance;

- It works well with digital banking and budgeting apps;

- It helps prevent overspending in a consumer-driven environment; and

- It strikes a balance between living in the moment and planning for the future.

Concluding remarks

The 50/30/20 rule is a mentality shift rather than merely a budgeting formula. You may develop a sustainable financial plan that enables you to pay for necessities, take pleasure in life, and accumulate money for the future by allocating your income among requirements, wants, and savings.

This rule offers a solid basis whether you’re just beginning your financial journey or are searching for a more straightforward approach to money management. As your financial situation improves, make any necessary adjustments to the percentages and maintain consistency.